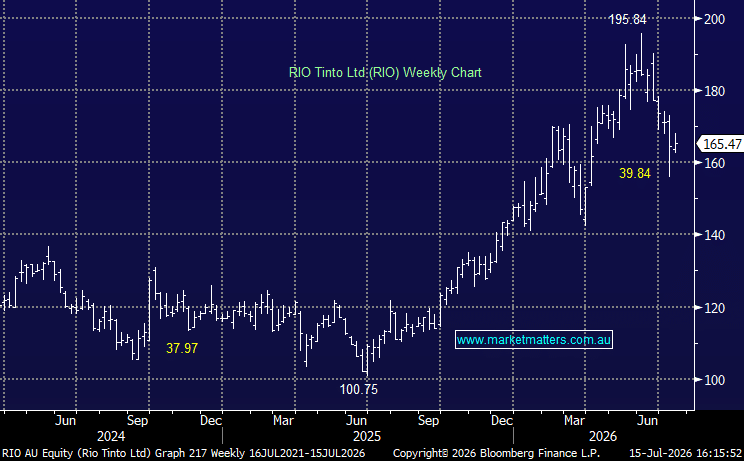

RIO +1.14%: delivered a mixed but broadly resilient second-quarter production update today, with a strong recovery across its Pilbara iron ore operations offset by weaker copper output following operational issues at Kennecott in the US.

Pilbara iron ore shipments increased 17% quarter-on-quarter and 6.8% year-on-year to 85.3 million tonnes, comfortably ahead of consensus expectations of 83.1 million tonnes. The improvement followed cyclone-related disruptions in the March quarter, with total group iron ore shipments reaching 88.8 million tonnes.

Second-quarter highlights:

- Pilbara iron ore shipments of 85.3Mt, up 6.8% year-on-year and ahead of expectations.

- Pilbara iron ore production of 83.5Mt, broadly flat year-on-year.

- Copper production of 213,200 tonnes, down 6.7% year-on-year and 7% quarter-on-quarter.

- Bauxite production of 15.2Mt, down 2.6%.

- Alumina production of 2.0Mt, up 10%.

- Aluminium production of 841,000 tonnes, broadly flat.

- Iron Ore Company of Canada pellet and concentrate production of 1.71Mt, down 31% and materially below expectations.

Copper production was the main area of weakness after unplanned outages at the Kennecott smelter in Utah forced the shutdown of a furnace that now requires rebuilding. The operation is expected to remain affected for around six months, although Rio maintained full-year copper production guidance of 800,000–870,000 tonnes.

Importantly, management materially reduced its copper C1 unit cost guidance to US30–50c/lb from US65–75c/lb, reflecting lower costs across the broader copper portfolio and stronger by-product credits. The Oyu Tolgoi underground expansion also remains on track to reach average annual production of around 500,000 tonnes of copper between 2028 and 2036.

Full-year guidance was otherwise unchanged:

- Pilbara iron ore shipments of 323–338Mt.

- Total iron ore sales of 343–366Mt, including 5–10Mt from Simandou.

- Pilbara unit costs of US$23.50–25/t.

- Copper production of 800,000–870,000 tonnes.

- Aluminium production of 3.25–3.45Mt.

- Bauxite production of 58–61Mt.

- Alumina production of 7.6–8.0Mt.

- Lithium production of 61,000–64,000 tonnes of lithium carbonate equivalent.

Rio said the Middle East conflict had caused no material disruption to production or outbound supply chains. However, higher diesel prices have increased Pilbara iron ore costs by around US80c/t over the past six months, highlighting some emerging inflationary pressure despite unchanged unit-cost guidance.

Overall, the June-quarter update was better than the headline weakness in copper suggests. The Pilbara rebounded strongly from the weather-affected March quarter, shipments beat expectations and full-year iron ore guidance remains intact. Kennecott is an operational frustration and will constrain copper output over the next six months, but the reduction in copper cost guidance and continued progress at Oyu Tolgoi are encouraging. With iron ore performing well and Rio continuing to build its exposure to copper and lithium, we remain constructive on the longer-term portfolio, although near-term earnings will remain heavily influenced by iron ore prices and the successful execution of Simandou.

MM is bullish RIO

Add To Hit List