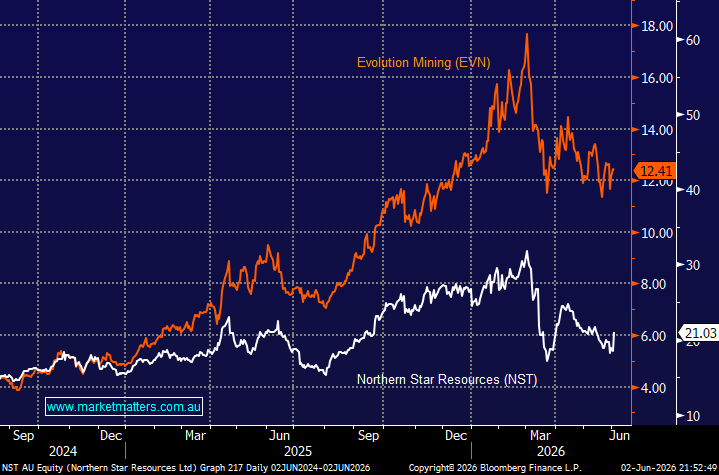

We had planned to take a closer look at our position in Evolution Mining (EVN) this morning, particularly why it has underperformed Newmont (NEM) by around 10% over the past three months. That underperformance raises an important question: are we positioned in the right gold stock to benefit from a potential recovery in the precious metal over the next 12 months?

However, Tuesday’s ~14% surge in Northern Star (NST), following news that activist hedge fund Elliott had taken a $1bn stake in the embattled gold miner, changed the comparison. Rather than looking at EVN versus Newmont, the more relevant question now is how Evolution stacks up against Northern Star.

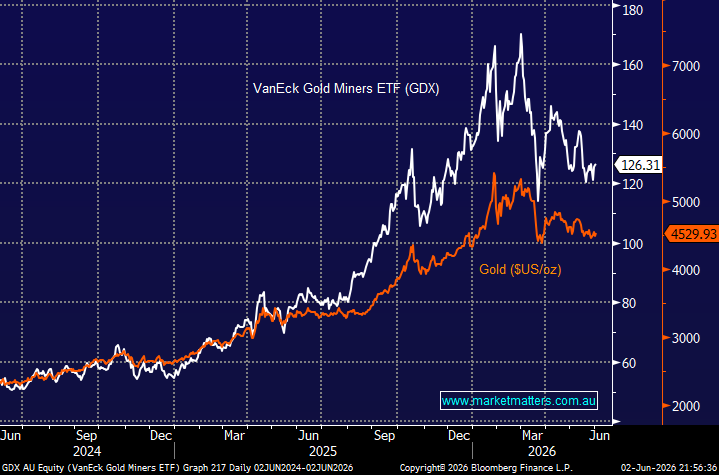

The gold sector became extremely crowded earlier this year as panic buying drove the precious metal above $US5,500/oz. As so often happens, the unwind was savage with indiscriminate selling washing through the stocks and the underlying precious metal. We believe both are now stabilising, although for gold to rebound back towards $US5,000/oz, the market needs a resolution to the US-Iran War, allowing bond markets to recover – weak bonds (rising bond yields) weigh on precious metals that pay no yield.

- We believe gold “is looking for a low”, but the war will determine its short-term swings.

chart

VanEck Gold Miners ETF (GDX) v Gold ($US/oz)

chart

VanEck Gold Miners ETF (GDX) v Gold ($US/oz)

Evolution Mining (EVN) is a world-class Australian gold miner with a valuable copper kicker, rather than a copper story with gold exposure. The primary driver of the stock remains the gold price, and on that front, we continue to like the setup. Gold has pulled back around 20% from its 2026 highs, but the medium-term backdrop remains supportive, with central bank buying, geopolitical uncertainty, sticky inflation and rising fiscal concerns all continuing to underpin demand for the precious metal.

EVN gives us leveraged exposure to any recovery in gold through a high-quality portfolio of Australian and Canadian assets, including Cowal, Ernest Henry, Mungari, Red Lake and Northparkes. The company has improved operational consistency, reduced balance sheet pressure and continues to generate strong cash flow at current gold prices. With revenue forecast to rise from ~$4.4bn in FY25 to ~$6.4bn in FY27, EVN still screens attractively on earnings and cash flow metrics.

The copper exposure is an important additional attraction, but we view it as upside optionality rather than the central investment case. Copper contributed around 30% of FY25 revenue, largely through Ernest Henry and Northparkes, giving EVN a differentiated profile versus most gold peers. Northparkes in particular has the potential to become a much larger contributor over the next decade, with throughput and copper production potentially doubling by FY35. If achieved, EVN’s copper output could exceed 100ktpa, around 25% above current consensus forecasts, and begin to rival the production profile of pure-play copper producers such as Sandfire.

Importantly, this copper exposure gives EVN an extra lever to value creation at a time when the medium-to-long-term outlook for copper is improving. Electrification, AI infrastructure, grid investment and constrained supply all support a positive structural view on the industrial metal. Every US50c/lb increase in the copper price could theoretically add around 50c, or ~4%, to EVN’s share price, assuming the gold price is unchanged.

However, we are not owning EVN because we want a copper stock. We are owning EVN because we want exposure to a quality gold producer at a time when we believe the gold price can recover, with copper providing a useful and potentially underappreciated kicker. That combination is attractive.

- We bought EVN in January after gold had been hit by more than US$1,000/oz, and frustratingly, the position is broadly flat at this stage. Still, with gold trading well below its highs, EVN generating strong cash flow and copper optionality continuing to build, we remain comfortable with the position and have no plans to exit.

Northern Star Resources (NST) is Australia’s largest gold miner, but it has been a serial underperformer following repeated operational downgrades and execution issues. Even after yesterday’s ~14% rally, the stock is still down more than 20% in 2026, compared to Evolution Mining (EVN), which is off just ~2%. Against that backdrop, it is easy to see why news of Elliott’s ~$1bn stake was so well received.

The market recognises that Northern Star owns a portfolio of world-class gold assets, but operational performance has fallen well short of expectations. In March, NST told analysts it expected to produce around 1.5 million ounces of gold in FY26, almost 20% below initial forecasts. That gap between asset quality and delivery is exactly the type of situation that attracts an activist investor like Elliot.

Elliott is pushing for a strategic review of the business, and Northern Star has already said it is open to constructive dialogue. The activist has also called for board renewal and the appointment of a “world-class external CEO” following Managing Director Stuart Tonkin’s decision to step down. That may encounter some resistance, but management has lost considerable investor support following the company’s poor performance, making NST a large gold miner ripe for change.

Elliott has criticised Northern Star’s recent track record, pointing to operational missteps, cost overruns and inconsistent strategic direction, which it believes have contributed to the company trading at a discount to global peers. It has also questioned management’s ability to successfully deliver key growth projects, including the KCGM Fimiston Mill expansion and the development of Hemi. Capital allocation has also been a focus, with Elliott arguing that more disciplined decision-making, stronger execution and improved governance could materially lift shareholder returns.

Importantly, Elliott is not a passive investor. It is one of the most effective activist funds globally, and its involvement brings real pressure for change. Whether the outcome is asset sales, a broader strategic reset, management change, improved capital discipline or even corporate activity, we would not bet against Elliott extracting value from Northern Star’s high-quality asset base.

Elliott is reportedly looking at a sale of all or part of NST as one potential path to unlocking value. That may or may not happen, but the message is clear: Northern Star’s underperformance and valuation discount are no longer being ignored.

- We like NST as a situation play in the gold sector. While execution risk remains, Elliott’s involvement changes the dynamic, and we see limited downside below $20, around 5% below yesterday’s close.

MM is bullish towards NST around $21

Add To Hit List

chart

Northern Star Resources (NST) v Evolution Mining (EVN)

chart

Northern Star Resources (NST) v Evolution Mining (EVN)