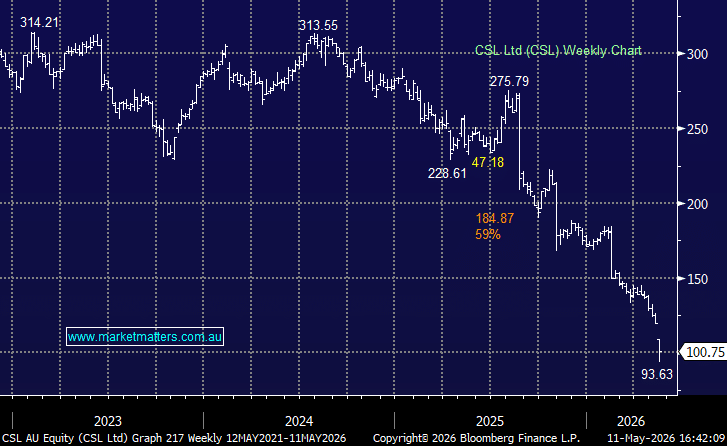

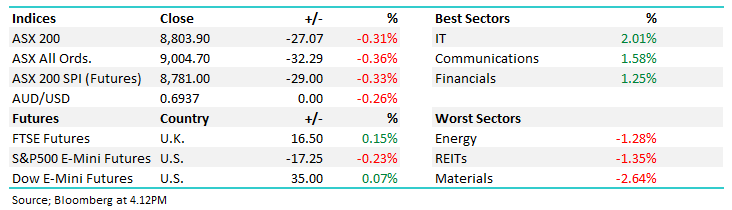

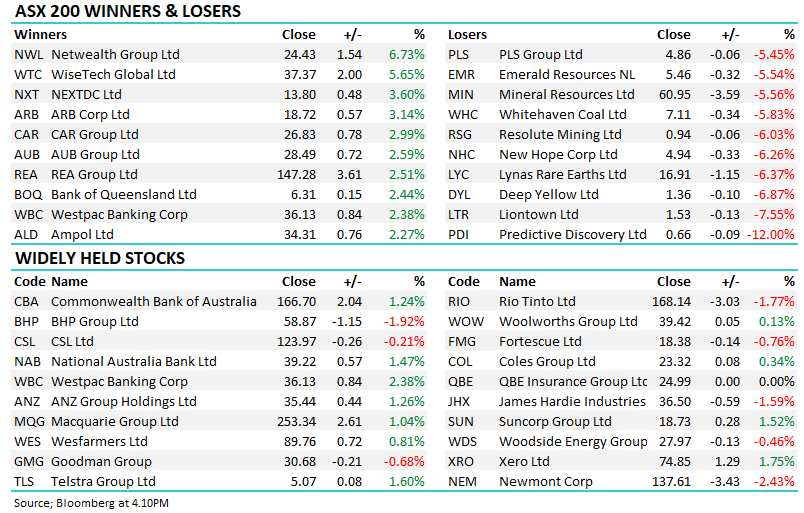

CSL –15.96%: collapsed after cutting FY26 guidance and flagging a further ~US$5bn in impairments, as the company acknowledged its turnaround is taking longer than expected following a strategic review by interim CEO Gordon Naylor.

- Revenue guidance: ~US$15.2bn vs ~US$15.8bn est.

- Net profit guidance: ~US$3.1bn vs ~US$3.3bn est.

- Additional impairments: ~US$5bn across FY26–27

The downgrade reflects ongoing pressure across several key areas of the business, including weaker immunoglobulin demand in the US, softer albumin pricing in China and continued challenges within the Vifor acquisition. Management also pointed to competitive pressures in plasma, where rivals have improved supply chains and product offerings, eroding CSL’s historic market leadership.

The update raises fresh questions around CSL’s post-pandemic growth profile and the returns generated from the Vifor deal, which has now been associated with multiple write-downs. While the company is targeting US$500–550m in annual savings by FY28, part of those savings will be reinvested back into growth initiatives, though with the company’s recent track record of allocating capital, this creates more questions than answers.

- Another poor update today from CSL, it’s 4th since August 2025.

MM remains neutral CSL ~$100

Add To Hit List