NST -18.75%: was hit hard today after they flagged softer-than-expected production through the March quarter, highlighting a combination of milling issues at Kalgoorlie and lower mining productivity at some operations. While the update points to ongoing operational challenges in the near term, we think the broader investment case is still okay given the strength in the gold price and the company’s medium-term growth pipeline.

NST said that January–February gold sales totalled ~220koz, though quarter-to-date production has been impacted by weaker milling performance at the Kalgoorlie Super Pit (KCGM) and reduced mining productivity across several operating areas, most notably at Jundee.

Back in January, the company already cut FY25 production guidance to 1.60–1.70Moz, reflecting some of these emerging operational pressures. Maintaining throughput at KCGM remains the key swing factor, with the current mill running close to its practical limits and proving difficult to keep at required levels consistently.

The good news is that the KCGM Mill Expansion Project remains on track, with commissioning expected in early FY27. That project should meaningfully lift processing capacity and improve operational flexibility at the asset, which remains one of the largest gold mines in Australia.

In the meantime, NST is undertaking an operational review at Jundee, aimed at improving efficiency and prioritising higher-margin ounces. As part of that process, management flagged the potential to redeploy surplus personnel and equipment to higher-margin operations, with changes expected to take place during the June quarter.

- More clarity should come with the March quarterly report on April 22, where the company plans to provide additional details on FY26 production and cost expectations.

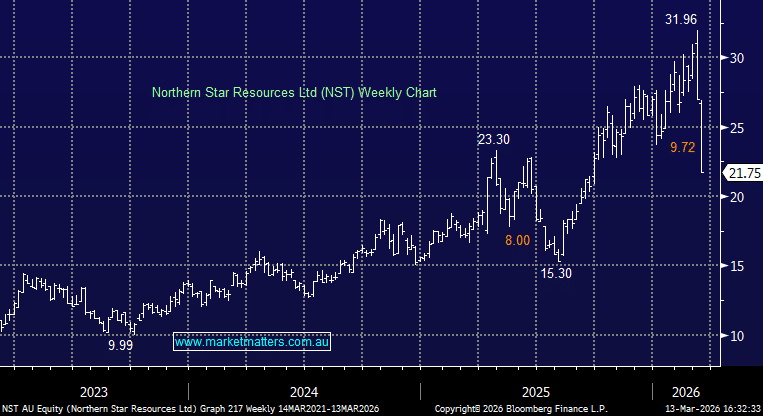

MM remains neutral NST ~$22

Add To Hit List