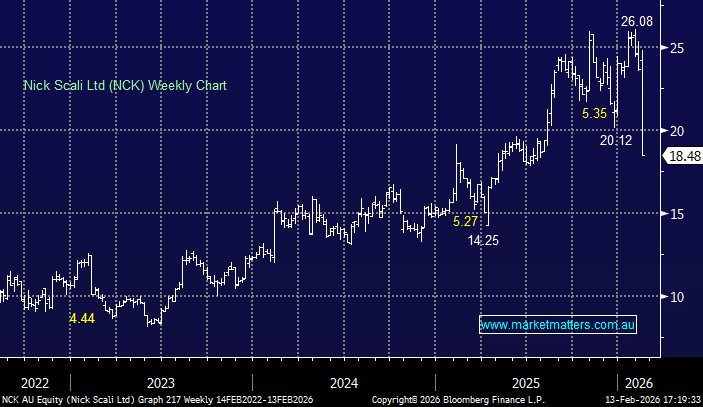

NCK -22.32%: Delivered a better-than-expected 1H result, but the stock was sold hard after a softer January trading update raised concerns about near-term demand for big-ticket items as interest rates rise.1H numbers:

- Net profit: $41.0m, +36% y/y – ahead of $37m consensus.

- Revenue: $269.3m, +7.2% y/y – ahead of $266m consensus

- Interim dividend: 39c, +30% y/y – ahead of the 33c consensus

However, January written sales are up just 3.1% in Australia/NZ (LFL +3.2%), which implies the order book is potentially falling short of consensus 2H26 revenue assumptions, particularly with interest rates moving higher. Furniture is a discretionary bellwether, and any hint of slowing demand tends to be punished – which was the case today.

CEO Anthony Scali pointed to November sales pulling demand forward, leaving January softer than usual. Foot traffic was down ~7% in January, but management argues March–April will be the real test of consumer resilience. Importantly, Australia/NZ revenue still rose 13.1% in the half, ahead of NCK internal expectations, and the UK story is improving, with LFL growth of 32% across converted Nick Scali stores highlights the benefit of the brand reset – albeit coming off a low base.

The UK business posted a $5.6m loss in the half but is nearing breakeven; scale remains the key lever. Long-term ambition remains 60–70 UK stores. The reaction mirrors broader pressure across discretionary retail. Temple & Webster sold off sharply on a weaker update this week as rising rate expectations and cost-of-living pressures are making investors far less forgiving on forward indicators, even when reported earnings are strong.

- Overall, this was a good result overshadowed by a cautious trading update. The sell-off reflects macro nerves, not execution issues.

MM remains long and bullish NCK in the Emerging Companies Portfolio

Add To Hit List