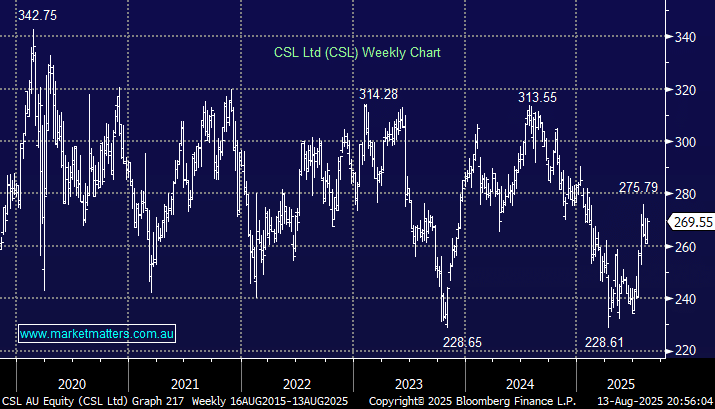

CSL advanced 2% yesterday in a weak market, leading the healthcare sector to a 1% gain. The $130bn global biotech has struggled since COVID but we believe its defensive nature and cheap valuation compared to history puts it in an excellent position to rerate on the upside.

- We are looking for CSL to initially test $280, but our preferred scenario is a retest of $300-310: we hold CSL in our Active Growth Portfolio.

MM is long and bullish CSL

Add To Hit List