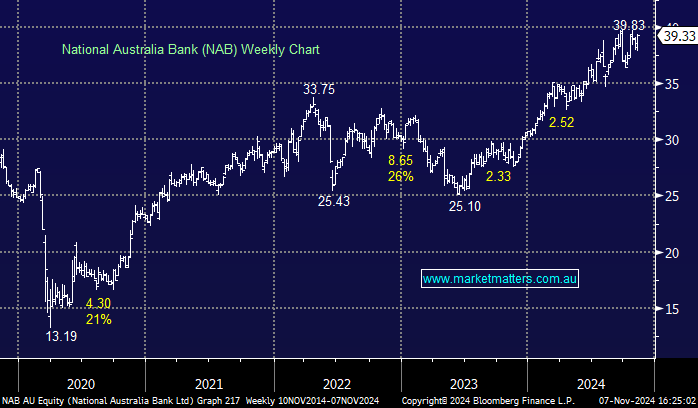

NAB +0.20% reported FY24 results this morning which were largely in line with consensus estimates:

- 2nd half net interest income of circa $8.3bn were flat from the prior half

- Net earnings of $7.1bn vs consensus of $7.06bn

- 2nd half dividend per share surprised slightly on the upside at 85cps vs. 84cps expected

The NAB result and guidance on the year ahead lines up with our thesis from back in August when we exited the stock. Outside of personal banking, the business saw decent growth in volumes. However, in a now saturated business banking sector where competition has ramped up meaningfully from the likes of CBA and other non-bank lenders, and while NAB called out a ‘more stable’ environment, it was interesting to note that business banking profitability declined HoH, with modest NIM pressure and bad debts trending higher.

Credit quality metrics over the period deteriorated and look to be worse than peers. With investment spend expected to increase significantly in FY25, a stretched 74% payout ratio and a full valuation, we don’t see the earnings profile of the business improving significantly enough to consider the stock.

MM remains neutral on NAB

Add To Hit List