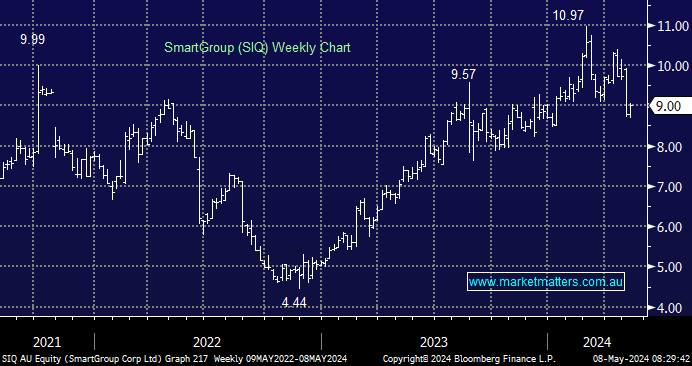

For those unfamiliar, Smartgroup is a $1.1bn leading provider of novated leasing within salary packaging and operates end-to-end fleet management services. They have a diverse and defensive mix of clients across Government and private enterprise, with a large proportion of their future growth underpinned by the take-up of Electric Vehicles (EV’s). While recent EV sales data has been on the softer side, the backdrop more broadly has been very strong with new car sales in April the best on record, driven by an easing in supply chains. This theme, along with an expanded range of EVs coming onto the market (electric SUVs for example) will be supportive of SIQ’s earnings growth, and therefore dividend growth over time.

- We have followed SIQ for an extended period as it made consistent new highs, however, an 18% pullback in price (excluding dividends) now presents a solid risk/reward buying opportunity, in MM’s view.

SIQ trades on 15.7x expected earnings, which are set to grow in FY24 at 15% while yielding 5.06% fully franked, although they have paid several special dividends in recent halves bumping the historical yield up significantly. Past FY24, growth will likely be moderate to high single digits, underpinning a similar increase in dividends.

A solid business that is capital-light and an alternate way of playing the global decarbonisation theme. One key risk to highlight is legislation, the provision of products and services within salary packaging administration and novated leasing is underpinned by benefits permitted under our taxation law, while changes around fringe benefits on EVs could also hurt sales in the segment, although we think Governments are focussed more on adoption than tax $$ at this point.

NB: SIQ hosts it’s AGM today.

MM has bought SIQ in the Income Portfolio under $9

Add To Hit List