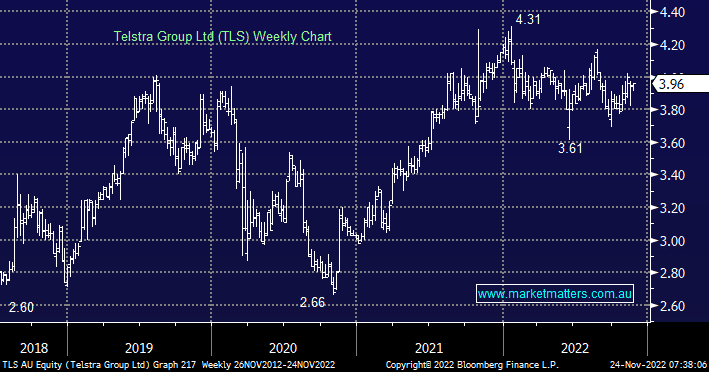

TLS has experienced a relatively quiet 2022, a win compared to many stocks, we like the major telco as a defensive play due to its relatively insulated earnings and a sustainable dividend of around 4.3% fully franked. As the Australian telecommunications industry evolves TLS is a relatively conservative play but it is more expensive than some of its peers, which we feel is not a problem at this stage of the cycle. In our opinion, the largest risk to the company’s earnings comes from heightened mobile competition but this is not a new factor – MM invested in the higher beta TPG Telecom (TPG) only to fall victim to a poor result i.e. TLS is the “keep it simple stupid” play for now.

- We like TLS around the $4 region eventually targeting a break of January’s $4.31 high.

NB, we currently hold TLS in our Active Income Portfolio from $3.43

MM is bullish TLS looking for a break of recent highs

Add To Hit List