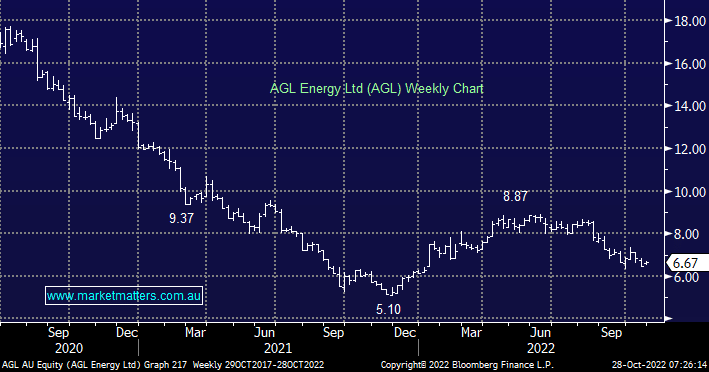

Mike Cannon-Brookes and the company’s exit plans from coal mean the electricity provider is being controlled by a very different mandate from most businesses on the ASX. As we’ve said previously we applaud the transition by all companies to a greener Australia but from a short-term valuation perspective it can be tricky and this is very much the case with AGL. AGL has actually been one of our strong performers in the Income Portfolio and we’ve recently re-entered the position having sold it above $8, and while earnings in the short term are hard to get a solid gauge on, the sum of the AGL parts we believe is worth more than the current share price implies. Overall we like the risk/reward around $6.50.

- Similar to ORG we like AGL’s projected yield above 5.5% for the next 12 months but the share price recovery could take some time.

MM is bullish AGL around $6.50

Add To Hit List