Hi Simon,

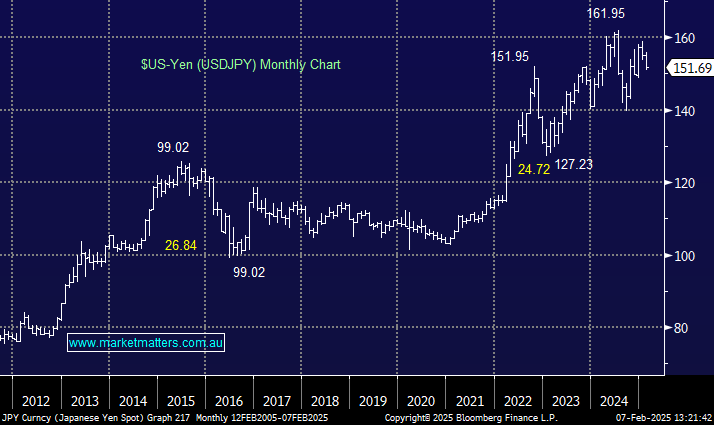

The Yen has been a fascinating currency over the last 6-months, the “yen carry trade” —a strategy where investors borrow in low-interest-rate yen to invest in higher-yielding assets—experienced a significant unwind in late July and early August 2024. The catalyst was a rate hike by the Bank of Japan (BoJ) in late July, which increased the benchmark interest rate to 0.5%, the highest level since the 2008 GFC. The BOJ had been hinting they would move but markets had been complacently short the Yen for years and just to ignore them, and crowded trades often lead to dramatic moves which is exactly what we witnessed.

- The BoJ’s “unexpected move” led to a rapid appreciation of the yen, rising +14% against the $US in just a few dramatic days. The surge forced investors to unwind their carry trades, as the rising yen increased the cost of yen-denominated borrowing, leading to significant sell-offs in global markets, including equities.

Now we have the Fed’s rate cutting cycle set for a prolonged pause while the BOJ are expected to hike another 1 or 2 times in 2025, arguably net supportive of the Yen. However, with so many variables on the horizon we would rather adopt a neutral stance around the 150 area, there are easier places to make money.

In terms of global indices, we remain net bullish through 2025 with the tailwind of, bar some Trump dally volatility, stable macro-economic picture and declining interest rates likely to remain supportive. However, while most indices are on the “rich” side we believe European and Australian equities will enjoy some performance catch up this year v they’re US peers, while for the brave we see upside in China facing indices.