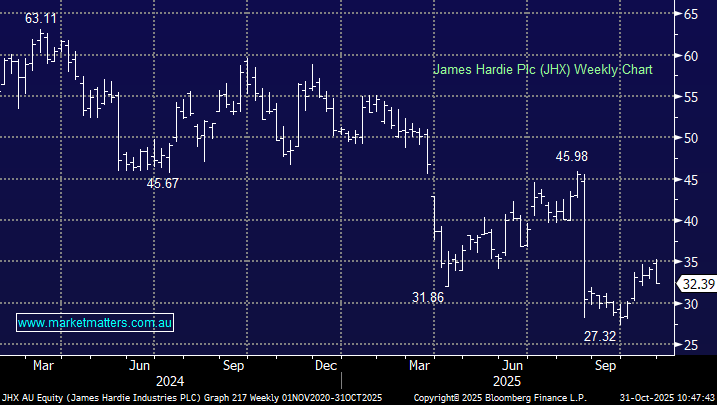

Hi Carl,

We think it was undoubtedly shareholders finally flexing their muscles over the almost uniformly “hated” acquisition of AZEK, and specifically, the way they intentionally circumvented share holder approval. The cash-and-share deal was valued at about $US8.75bn, including AZEK’s net debt. We thought the actual idea for AZEK makes sense, just the price paid and the way it was executed was poor.

- JHX paid a 26% premium to AZEK’s average price (VWAP) over the 30 trading days prior to the announcement – very rich considering the lacklustre US construction industry.

- Also, AZEK’s valuation multiple (EV/EBITDA) was well above JHX’s own multiple, meaning Hardies was buying at a higher price than it trades at itself.

Strike one, JHX paid too much – however, what rankled most shareholders, including MM, was the stealth like manner of the purchase:

- They adopted a US merger structure where the merger agreement stipulated that AZEK shareholders must vote to adopt the merger, but JHX shareholders did not.

- JHX obtained a waiver of the shareholder-approval requirement under the Australian Securities Exchange (ASX) Listing Rule 7.1/7.2, which normally limits the amount of equity a listed entity can issue without approval.

- The plan to shift primary listing or increase U.S. index inclusion raised concerns about reduced Australian shareholder oversight and weaker governance protections under U.S. listing rules.

Under normal due process this deal would have been knocked back. However, by avoiding a JHX shareholder vote, many felt existing shareholders’ interests and rights were being diluted without their input as the issuance of new shares to fund the acquisition (~35 % of existing capital) significantly diluted existing shareholders, yet they didn’t get a say.

Strike two, it was a “sneaky” deal, executed and communicated poorly – and we’re not vaguely surprised some directors were kicked into touch.