Hi Jacqui,

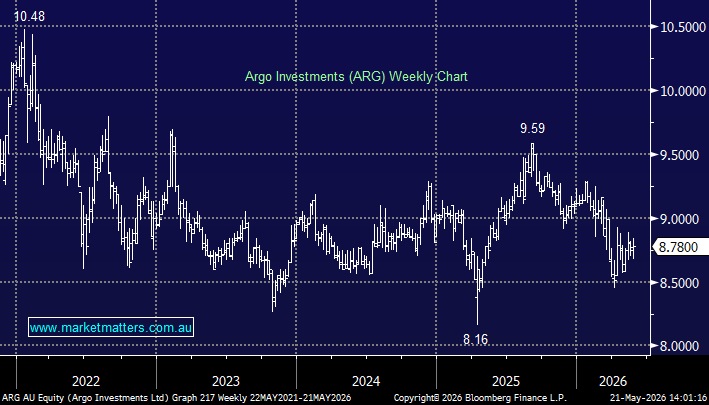

Interestingly, the second question today on LIC’s with a similar level of disappointment. The crux of it comes down to portfolio performance. WAM (discussed in another question), ARG and AFI have had a period of weak performance, hence investors have lost some faith.

We covered AFI a few months ago here, which might also give you a bit more insight. AFI remains one of Australia’s best-known listed investment companies (LIC), offering investors a low-cost, internally managed portfolio of predominantly blue-chip Australian equities with a strong focus on long-term investing and fully franked income. The stock yielded ~5.2%, fully franked over the last 12-months and, importantly, trades at an ~13.8% discount to NTA despite historically averaging a modest premium. The reason for the discount is weak performance. Over the past 5 years, they have underperformed the market by ~6% annually, trailing the markets return by ~7.5% in the past 12 months (inclusive of dividends).

Performance has been hurt by weak returns from several large holdings and limited exposure to high-growth sectors and gold, highlighting the inherent rigidity of low-turnover, value-oriented strategies. Still, for patient long-term investors who believe in the classic buy-and-hold LIC model, the current discount to NTA provides a potentially attractive entry point, particularly if portfolio performance improves and the discount begins to close.

The biggest impact on LICs has been the rise of ultra-low-cost ETFs, which offer diversified ASX exposure without the risk of persistent NTA discounts, pulling investor flows away from LICs.

That said, we think the current discounts being offered by the larger LICs make them attractive from a takeover perspective – maybe by a large super fund. Not sure of the mechanics around this, but buying a large portfolio of ASX companies at a discount to their current value makes a lot more sense than paying a premium (as discussed in another question on WAM today).

In terms of size, AFI & ARG are big, and this should not be an impediment as it is with other smaller LICs. It’s just they seem to be losing out currently to ETFs. We see value in AFI and ARG here, though performance of their underlying portfolios needs to improve.