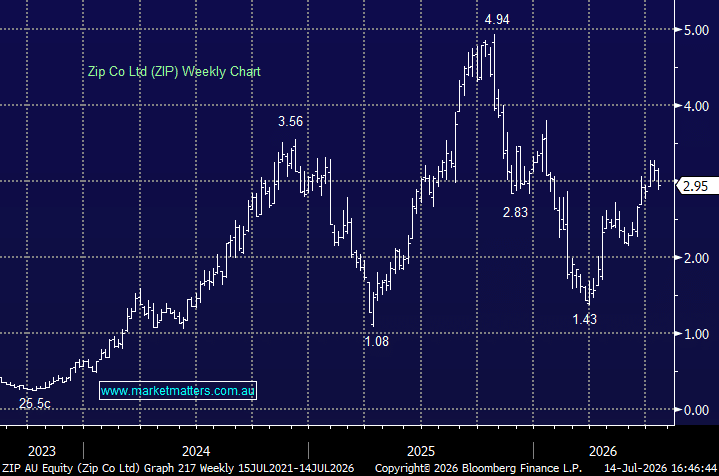

Zip remains one of the stronger performers in the Market Matters Emerging Companies Portfolio, with the share price rallying materially since our entry in mid 2025 at $1.87. We continue to like the company’s improving earnings profile and exposure to structural growth in buy now, pay later, although we trimmed the position last week following the strong run.

The key attraction remains Zip’s US business, which has become the primary driver of group growth. In a recent note from UBS, where they upgraded their price target to $4.10 (from $3.10) they detailed their expectations for US transaction volumes in constant currency to increase by around 40% in the June quarter, supported by continued customer growth, higher spending per customer and a resilient US consumer. Importantly, around 65–70% of Zip’s US transaction volume is estimated to relate to non-discretionary spending, making the business somewhat more defensive than the BNPL label might suggest.

Zip is also demonstrating meaningful operating leverage. Group transaction volumes are forecast to rise by ~27% in FY26, while cash EBTDA is expected to increase by more than 50% to at least $260m. UBS forecasts earnings per share growth of ~36% in FY27 and ~34% in FY28 as revenue growth, disciplined costs and lower funding expenses flow through to the bottom line.

Recent refinancing activity is another positive. Lower interest expenses, combined with the potential for US interest-rate cuts, have prompted UBS to lift its FY27 and FY28 cash EBTDA forecasts by 11% and 12%, respectively. This is important because Zip is moving beyond a simple volume-growth story and increasingly demonstrating its ability to convert scale into sustainable earnings and cash flow.

The Australian business remains the softer part of the equation. Customer and app engagement trends have continued to decline locally, and UBS expects only modest Australian transaction growth in FY27. Credit quality also warrants attention, with net bad debts forecast to remain near the upper end of management’s 1.5–2.0% comfort range. However, Zip retains the ability to adjust approval settings and credit limits as conditions change, providing an important lever to protect returns.

Overall, Zip’s turnaround has progressed faster and more successfully than many expected, with the US business delivering strong growth while profitability continues to improve. We remain positive on the medium-term outlook and believe the company has further earnings upside as BNPL adoption increases and funding costs ease. However, after the significant appreciation since our entry, the risk-reward has become less compelling in the immediate term.

We trimmed the holding last week to manage position size and lock in some gains, while retaining meaningful exposure to a business we continue to like.

MM remains long & bullish ZIP ~$3.00

Add To Hit List