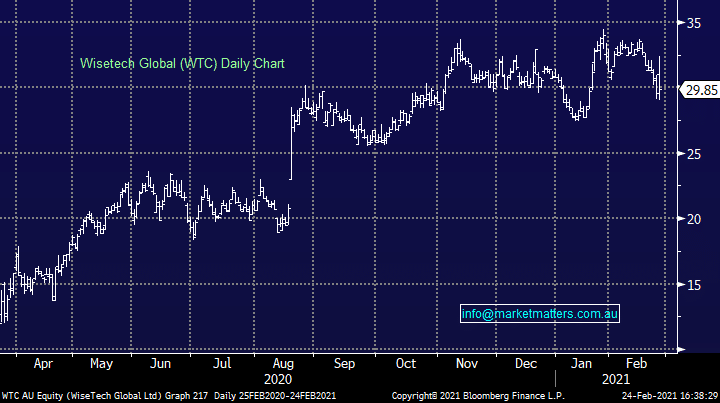

WTC released its 1H21 result and overall, it was a strong revenue number while they also did well on cost performance. These guys were impacted by COVID however the recovery is now well under way . FY21 revenue guidance was unchanged, but EBITDA guidance was kicked up by increased +6% and that’s what’s underpinning a slight uptick in the shares today, although they have come well off early morning highs. In terms of the numbers, FY revenue should come in between $470-510m (9-19% growth) and the increased EBITDA guidance implies to $165-190m (vs $155-180m prior).

WTC still remains expensive and opaque, we have no interest around $30

Add To Hit List