WTC +11% rallied today after management delivered one of the most forceful, and explicit, embraces of AI we’ve seen from an ASX-listed software company – an example of leaning heavily into AI rather than approaching it with incrementalism – a theme we discussed on our recent webinar (here).

1H26 Highlights

- 1H NPAT: $114.5m (+2% YoY)

- Revenue: $672m (+76% YoY), boosted by the E2open acquisition

- Organic revenue growth: ~7%

They also reaffirmed FY26 guidance for:

- EBITDA +44% to +53% to $550 million to $585 million

- Revenue +79% to +85% to $1.39 billion to $1.44 billion

- Ebitda margin 40% to 41%

On the conference call post the result, New CEO Zubin Appoo made it clear that AI is not a threat to WiseTech’s model, but a tool to fundamentally reset its cost base and development economics. The headline move is significant: up to 2,000 roles (~30% of the workforce) will be eliminated over the next two years under what management calls a “deep AI transformation”.

Appoo described AI-driven productivity gains that are already reshaping the business – projects that once took six to seven months can now be completed in a day, while rolling out global customs capability in new countries is happening six to seven times faster than before. The implication is clear: fewer people, faster product delivery, and materially better operating leverage.

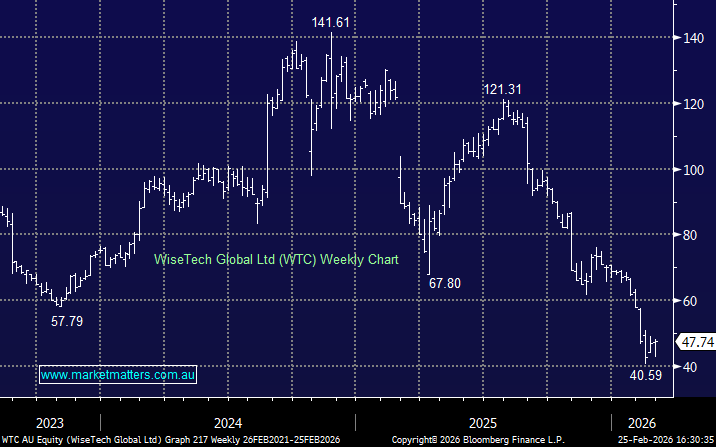

WiseTech’s share price has been under intense pressure this year (down ~37% pre-today) on fears that AI could commoditise freight and logistics software. Today’s update flipped that narrative. Rather than being displaced by AI, WiseTech intends to internalise the productivity benefits, stripping out cost and embedding its platform deeper into customer workflows.

Management articulated what AI meant for WTC very well:

- The era of manual coding as the core act of engineering is “over”.

- In some functions, particularly customer service, up to half of roles will disappear.

- AI agents will increasingly sit alongside specialist humans, supervised rather than replaced entirely.

They also pushed back on the idea that WiseTech is vulnerable to the classic “per-seat pricing” AI disruption seen in other software models. He argues CargoWise is mission-critical infrastructure, embedded at the centre of global trade flows, not an overlay that can simply be swapped out.

While near-term earnings growth remains modest, we think the market will now start to look through FY26, focusing on what a structurally lower cost base could mean for margins over the medium term. If WiseTech can execute on these productivity gains without damaging customer experience or innovation, the margin upside could be substantial.

- A good update, one that shows WTC is leaning heavily into AI – exactly what we were looking for.

MM is bullish WTC ~$48

Add To Hit List