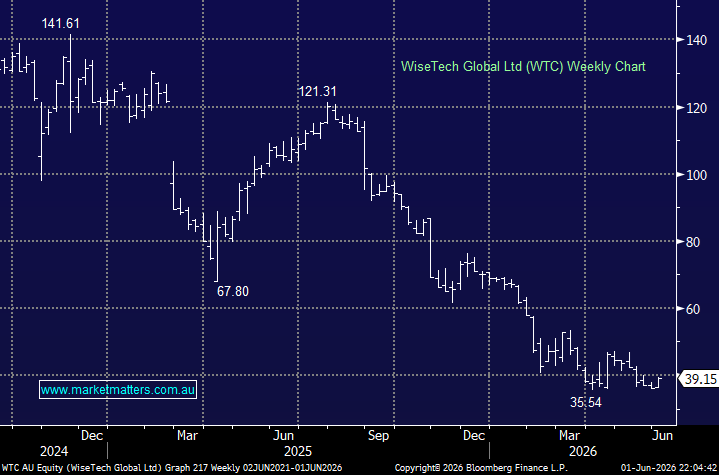

WiseTech was once widely regarded as one of Australia’s highest-quality software businesses, providing mission-critical logistics software through its flagship CargoWise platform, which helps global supply-chain operators manage the movement of goods across international trade networks. However, Richard White’s behaviour and the governance fallout over the past year have understandably led many investors to question that premium-quality label. Still, after a horrible 12 months for the stock, we believe there is clear value emerging in the business.

At its core, WiseTech remains a high-quality software company. The business benefits from powerful network effects, deep integration into customer workflows and a vast proprietary dataset built over decades of global trade activity — all increasingly important when thinking about software in the new world of AI. The market’s key concern has been that advances in automation and generative AI could erode CargoWise’s value proposition by making documentation, compliance, workflow management and other administrative functions easier to replicate.

Adding fuel to these concerns was news that DSV, one of WiseTech’s largest and most important customers, has decided to transition away from CargoWise following its acquisition of DB Schenker. DSV is one of the world’s largest freight forwarders and is moving its Air & Sea transport management operations onto DB Schenker’s proprietary Tango platform. This is clearly a negative headline for WiseTech, but DSV is also in a very different position to most customers, having acquired a sizeable competing platform with DB Schenker. We do not think most CargoWise customers have the same luxury, nor the scale, cost appetite or operational flexibility to replicate such a move.

Logistics is a highly complex, regulated and interconnected industry where data quality, integration and operational reliability matter enormously. As a result, we view WiseTech as more likely to be an AI beneficiary than a victim. Its enormous logistics dataset, entrenched customer relationships and central position within global supply chains provide a strong foundation for embedding AI into the platform, potentially improving productivity, automation and customer outcomes while further strengthening its competitive moat. The company has already said AI will allow it to reduce its workforce by around 30%, which, if executed well, would have a meaningful positive impact on margins and the bottom line.

With the stock now trading around 60% below its five-year valuation average — albeit from very elevated growth multiples — the risk/reward looks increasingly appealing in our opinion. Governance concerns remain, and the DSV/Tango development is not immaterial, but the market appears to be pricing in a far more challenged future for a business that still has significant structural advantages.

- We can initially see 30-40% upside for WTC from below $40 – MM owns WTC in the Active Growth Portfolio.

MM is long and bullish towards WTC around $39

Add To Hit List