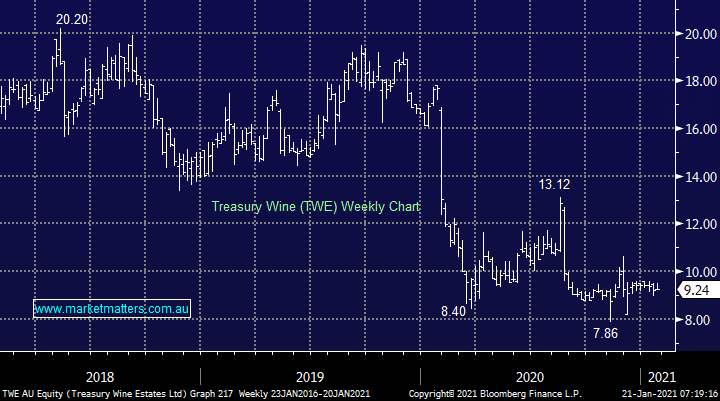

TWE has been under significant pressure with a wine glut in North America and the painful impact of a trade war with China but investors should look through these clouds because suitors will as they asses the companies value around $9. Also, even if someone doesn’t lob in a bid for the entire company the prospect exists to sell off parts of the business with Penfolds alone arguably worth today’s market cap of TWE. This is the sort of buy and restructure strategy PE firms love.

The companies delivered the combination of underwhelming results / downgrades and it’s a situation stock courtesy of China but again after falling more than 50% I’m sure its catching some long term investors’ attention.

MM likes TWE as an aggressive play

Add To Hit List