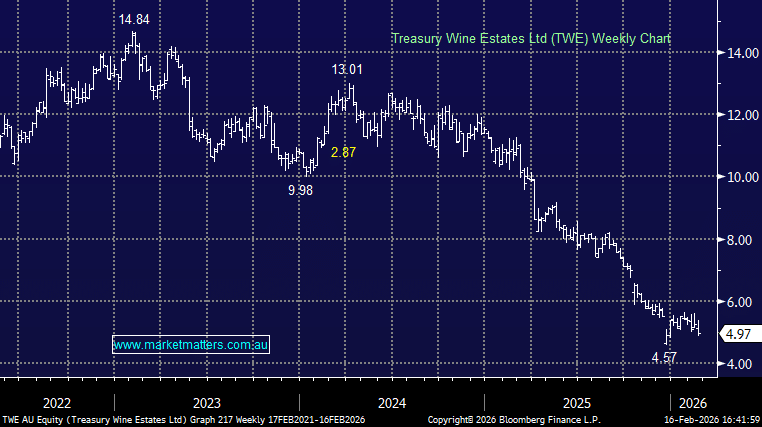

TWE –5.15%: The result today largely confirmed last week’s pre-announcement, but it was still a difficult read, with weak Americas performance and a major impairment charge driving a large statutory loss. The market’s attention is firmly on the outlook rather than the headline loss, with investors focused on cost-out execution, balance sheet repair and whether momentum can stabilise in the Americas and China over the next 12–18 months.

- Revenue $1.31bn, -17% YoY (vs $1.38bn est.)

- EBIT $236.4mn, -40% YoY (vs $231mn est.)

- Impairment/material items charge $770mn

We’ve been neutral on TWE for some time, and this update doesn’t materially change that stance. The stock looks cheap, but the structural headwinds — a world that is simply drinking less, stronger competition, and heightened sensitivity to China — are not going away quickly.

While TWE may be in the “eye of the storm” short term after the recent overhaul and write-downs, it remains a difficult stock to grapple with, until earnings stabilise and sustainable top-line growth returns.

MM is neutral toward TWE ~$5

Add To Hit List