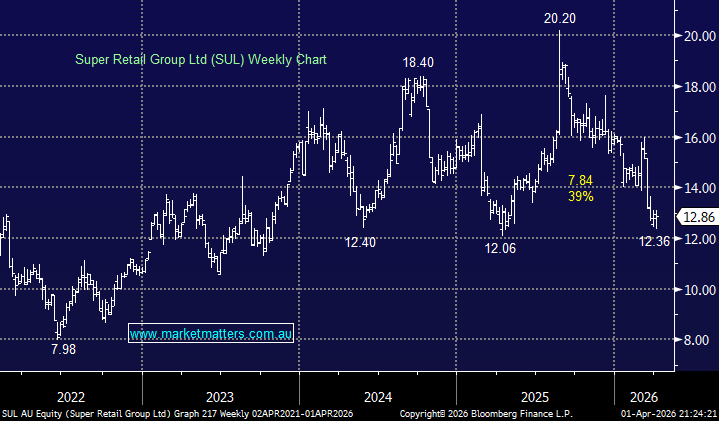

SUL delivered a sold 1H result in late February Here, pushing the stock up over 8% which importantly pointed to a clear improvement in trading momentum early in the second half, before the war! The retail sector has struggled through March as the war pushes up inflation concerns, bond yields and the prospect of three RBA rate hikes before Christmas. We believe markets are pricing in a worse case scenario and a bounce to $16 feels likely after an almost 40% decline from its 2025 high.

NB We prefer JB Hi-Fi in the local retail space though SUL is a strong alternative after its solid 1H result, if investors become confident in a recovery in the retail sector post-war.

- We like the risk/reward towards SUL, targeting the $16 area, or ~20% higher.

MM is bullish SUL around $12.80

Add To Hit List