Suncorp’s 1H result out this morning looks ugly on the surface, but importantly it was broadly consistent with the softer outcome expected. Elevated natural hazard losses and investment mark-to-market headwinds (due to higher rates) has impacted the profit line, although they maintained full year guidance.

The headline miss was always likely:

- 1H26 Cash profit of $270m, -67% YoY

- Interim dividend: 17c (down from 41c) – this was a bit light on even vs recently revised forecasts

Natural hazard costs came in $453m above allowance, totalling $1.3bn. This was largely known, noting UBS were forecasting a hit of $580m above allowance. Despite the headline weakness, the core insurance metrics were stable, which is the key takeaway.

- Underlying insurance trading ratio: 11.7%, essentially unchanged YoY

- Gross Written Premium: $7.69bn, +2.7% YoY

- Expense growth: +4.4%, with scope for improvement into FY26

There were nine declared events in the half resulting in ~71,000 claims for a net cost ~$1.3bn. This is abnormal but obviously par for the course of being an insurer. Importantly, management did not change guidance:

- FY26 insurance trading ratio still targeted at the top end of 10–12%

- FY26 natural hazard allowance lifted to $1.77bn

- Buyback: up to $400m to be completed by end-FY26

From here, near term earnings are going to remain highly sensitive to weather, but Suncorp is better capitalised and better priced than in past cycles.

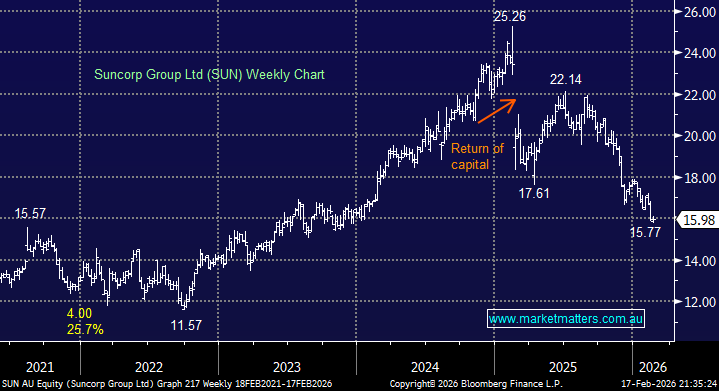

- This was not a good result, but nor was it a surprise, with SUN currently priced accordingly. We have recently bought SUN in the Active Income Portfolio.

MM is long and bullish SUN ~$16 for Income

Add To Hit List