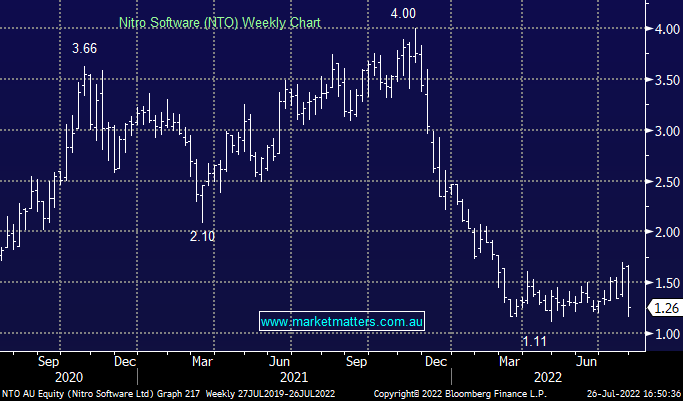

NTO -22.7%: the signature and document productivity business was hit hard following their 2Q update today. Annualized Recurring Revenue (ARR) ended the period at $US51.5m, up 11% in the period, largely driven by an increase in services offered to existing clients. The company noted that sales cycles had lengthened, another way of saying new clients have been hesitant to spend money to integrate Nitro’s software. As a result, the company downgraded ARR guidance from $US64-68m to $US57-60m, an 11% cut, with the market particularly concerned with the reduction in expected revenue synergies from the Connective acquisition from $US2.5m to just $US1m. They did maintain revenue guidance, and improved operating EBITDA loss expectations by 30% to $US10-13m on the back of $US5m in planned cost savings to come through in the second half.

MM is reviewing its NTO position after a poor update

Add To Hit List