We all understand the insurer’s business model, most of us pay them a lot each year! They collect premiums upfront and pay claims later. The gap between collecting the premium and paying the claim is called the float — and crucially, that float is invested. For a large general insurer, the float can be enormous relative to equity. Warren Buffett spent decades explaining why insurance is such a powerful business model when run well — you’re essentially being paid to hold someone else’s money, then investing it. Most insurer investment portfolios are dominated by bonds and cash, typically 70–80% fixed income; hence, higher bond yields equal higher returns.

For a company like IAG or Suncorp, its investment portfolio is measured in the billions. Moving from a 1.5% yield to a 4.5% yield on $10 billion of invested assets adds ~$300 million in pre-tax income annually, often more than the underwriting profit itself. This happened in real-time from 2022 onwards and is why insurance stocks were among the standout performers globally in 2023–2025. As older low-yielding bonds mature and are reinvested at higher rates, the portfolio yield continues to improve for years, even if the RBA doesn’t raise rates further.

- The earnings tailwind from high rates is not a one-off for insurers; it compounds over 3–5 years as the book rolls over. Today, many insurers are still in the middle of this process.

An additional tailwind for the sector is that inflation justifies premium increases, and regulators generally accept them. Building costs (home insurance), car replacement costs (motor), and medical costs (health insurance) have all risen sharply, and insurers were able to pass these through in higher premiums. QBE Insurance (ASX: QBE), IAG Insurance (ASX: IAG) and Suncorp (ASX: SUN) all pushed through significant rate increases from 2022 to 2025. In many lines, premiums grew faster than claims, expanding underwriting margins.

- It’s not all good though. Higher inflation leads to higher repair costs, which does off-set some of the benefit, though net-net, higher yields provide a tailwind for the insurers that we shouldn’t ignore.

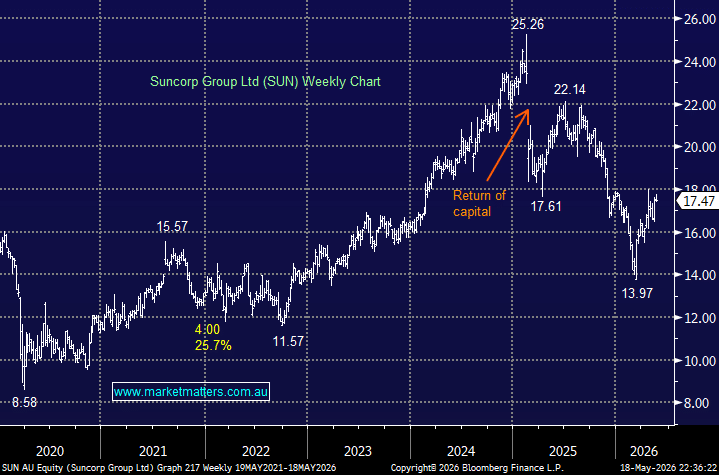

Our top pick to gain exposure to the insurance sector at current prices is Suncorp, supported by a ~5% fully franked yield, but it’s a close call between it and rivals QBE Insurance and IAG Insurance (ASX: IAG) – MM owns QBE in the Active Growth Portfolio, and Suncorp in the Active Income Portfolio.

- We can see Suncorp outperforming the index and banks in the coming years.

MM is long and bullish on Suncorp around $17.50

Add To Hit List