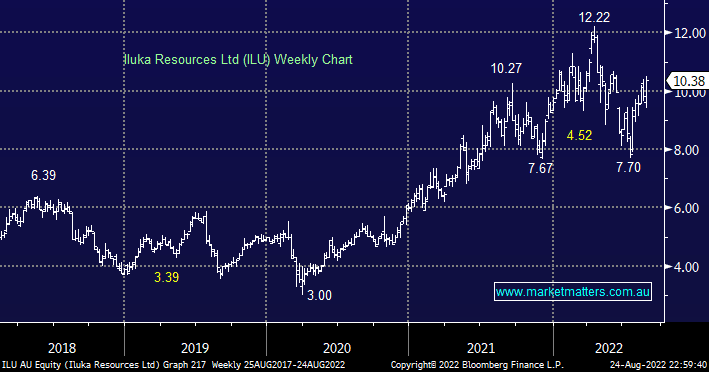

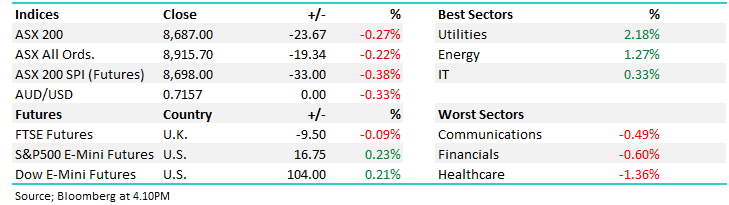

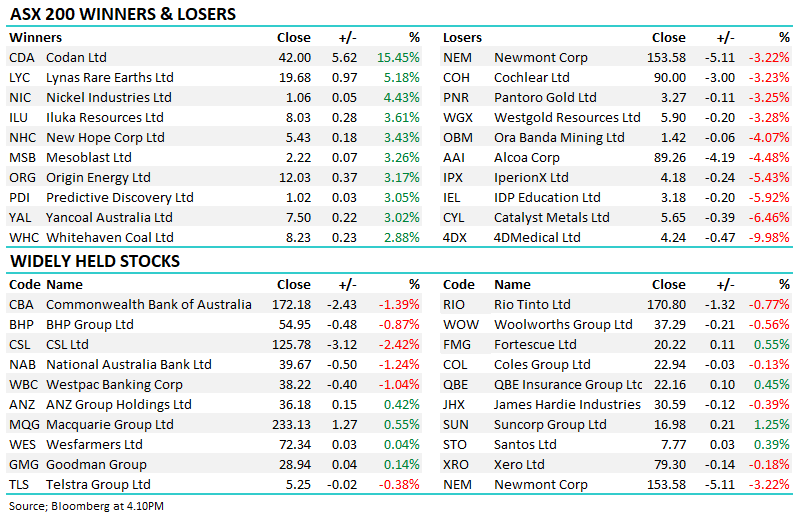

ILU has recovered strongly from its mid-July low and we can see a break of $12 over the coming months following the company’s strong quarterly update in July. This leading mineral sands operator has enjoyed rising prices due to elevated demand & tight supply for products like paints, tiles and batteries. We believe this stock is far better placed to hide from the Chinese property implosion than purer iron plays such as RIO mentioned earlier. Yesterday saw the stock soar almost 10% after delivering a stellar half-year result which included free cash flow of ~$350mn and a 25c fully franked dividend being paid on the 5th of September.

Importantly this year has seen ILU announce and commence delivering on two major corporate moves, the first a pivot into Rare Earths, aka Lynas (LYC), which will attract attention from ESG focussed investors and the 2nd being the demerger of Sierra Rutile (SRX) which was acquired in 2016 as the company focuses on its Australian mineral sands and the new rare earth businesses. As an aside, we are running the ruler over SRX for our Emerging Companies Portfolio.

- We believe ILU is cheap trading on an Est P/E of 7.9x for 2022 and we like the company’s direction as its moves into rare earths i.e. LYC trades on a valuation almost double that of ILU.

MM is bullish ILU ultimately looking for a break of its 2022 high

Add To Hit List