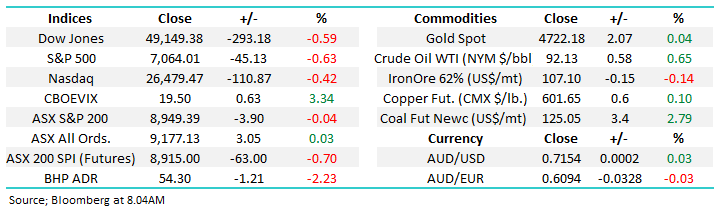

US stocks and bonds both edged higher on Monday ahead of some major earnings this week including Netflix, Tesla, and Johnson & Johnson yet markets are extremely comfortable at current levels with the VIX (Fear Gauge) dipping under 17%. Analysts expect earnings to decline for the 2nd straight quarter logging the steepest quarterly decline since 2020, by definition, this leaves room for surprises on the upside as we saw from the banks last week.

- No change, we continue to look for US stocks to push marginally higher over the coming weeks with our target for the S&P500 now ~5% higher.

- From a defensive standpoint a “failed pop” above 4200 would be of concern.

MM remains mildly bullish toward US stocks through April

Add To Hit List

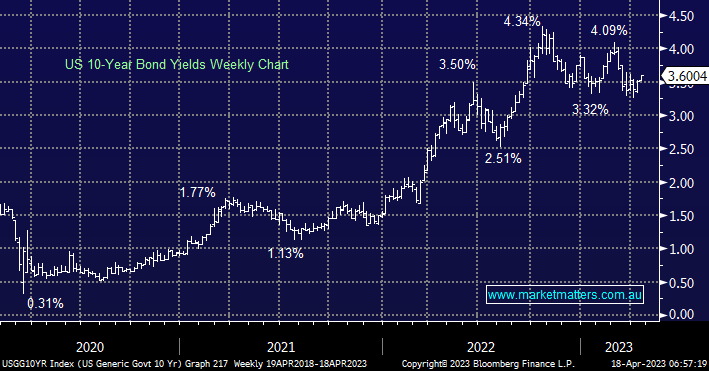

Investors have become almost fixated on the path of interest rates with many latching onto the Fed’s recent rhetoric and now looking for another +0.25% hike in May. The US 10-year yield has now risen for 7 of the last 8 trading sessions, not surprisingly starting to slow the outperformance of growth/tech stocks in the process.

- We cannot see a great deal of downside for bond yields short term which makes recent firmness across equities all the more impressive.

MM remains mildly bullish toward US stocks through April

Add To Hit List