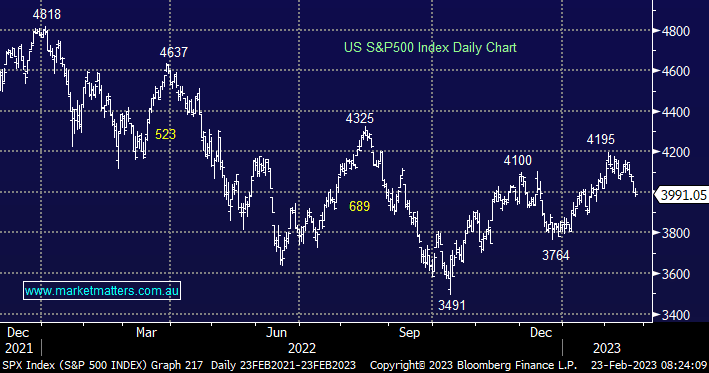

US stocks closed mixed overnight with the Dow falling -0.3% while the NASDAQ edged higher +0.1%, concerns that rates will stay higher for longer continue to weigh on investor sentiment – several officials said an “insufficiently restrictive” policy could stall the recent progress of tempering inflation. The latest minutes suggested the Fed is now prepared to hike rates to above the 5.1% rate forecast in December i.e. its sounds like they feel they’re losing the battle!

- Our preferred scenario remains the S&P500 will eventually test the 4300 area, now ~5% away.

MM remains cautiously bullish on US equities through February/March

Add To Hit List

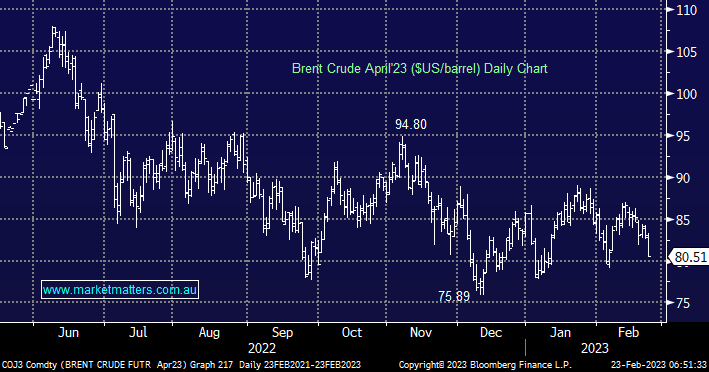

Crude oil has been drifting lower since last June with supply constraints due to the Ukraine-Russia war fully understood and built into prices, they are now trading slightly below where they were when Russia invaded its neighbour although prices had been edging up into that fateful day in late February last year.

- Crude oil has been trading around current levels since mid-2021 suggesting it’s where supply and demand are currently balanced, the obvious risk to crude prices would be a resolution in the war – something we are all hoping for.

MM is neutral crude oil ~$US80/barrel

Add To Hit List