The ASX200 slipped -0.55% yesterday but once we take out the huge dividends delivered to happy investors the market actually hardly moved e.g. BHP Group (BHP) $2.74, CSL Ltd (CSL) $1.64, Woolworths (WOW) 55c and Perpetual (PPT) 96c. Importantly these funds will drop into shareholders bank accounts around the end of September / start of October providing yet another tailwind for this already resilient market i.e. a significant portion of investors simply reinvest their dividends back into the market aka compound interest – it’s a tough time for the bears!

The “buy the dip” characteristic appears to regularly coincide with Gladys 11am COVID presentation, yesterday the market bottomed at 11am almost to the minute, it appears the news of a record number of fresh cases for NSW combined with our initial vaccination rate soaring through 70% provides the optimum backdrop for stocks. Local 10-year bond yields continued to drift lower breaking under 1.2% yesterday, even as we the country looks to reopen in the coming months – I wish I could borrow money at 1.2% for the next decade!

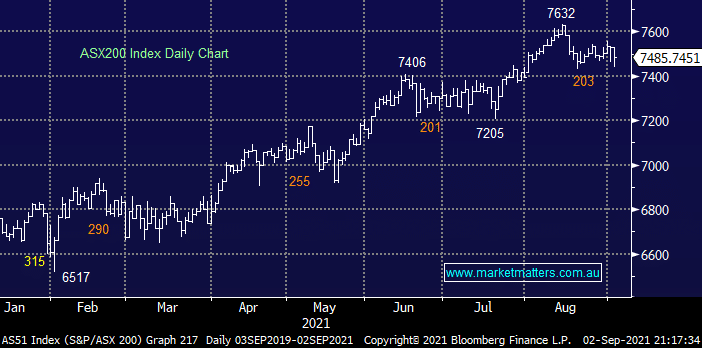

A few weeks ago we laid out MM’s 2 preferred paths for the ASX200 and after over 10-days of “sideways chop” we remain happy with both scenarios, hopefully we will see the market show its hand fairly soon although if we follow the action in June / July patience will be needed:

- The markets completed another 200-point correction as we did in June / July and the uptrend will resume in September / October.

- Alternatively this pullback will extend back towards 7300 and resemble the two in Q1.

Either way MM is bullish and we’re looking for good risk / reward opportunities to increase our exposure to both the overall market and specific stocks / sectors. Our overriding view is the market will be higher in 6-months’ time hence the greatest risk to investors is moving underweight equities and missing any further gains. As we’ve said a number of times the main game in 2021 remains stock / sector selection while maintaining a core bullish stance.

US stocks edged higher overnight with tonight’s key Jobs Report overshadowing the day, the S&P500 made another record high even with tech drifting lower. The SPI futures are pointing to an open up around +0.2% this morning with energy stock likely to shine but overall a quiet session feels likely.

MM remains bullish the ASX and keen buyers of pullbacks

Add To Hit List