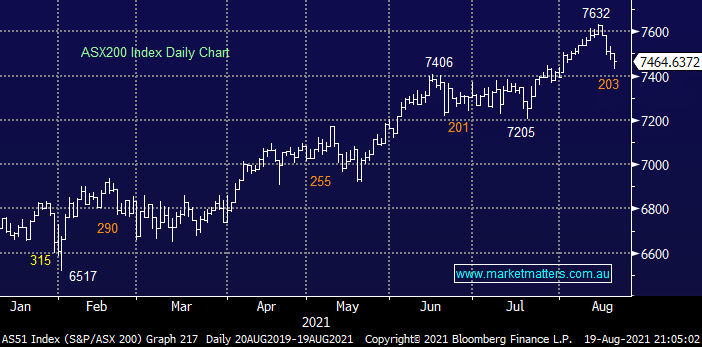

The ASX200 fell another -0.5% yesterday even with the number of winners & losers evenly balanced, however the influential Resources Sector was again smashed with heavyweights BHP Group (BHP), RIO Tinto (RIO), Independence Group (IGO) and Fortescue Metals (FMG) all falling by over 5%. Iron Ore and copper were down heavily during our time zone and not surprisingly this flowed into aggressive selling across ASX related stocks.

Rotation on the stock and sector level continues to dominate proceedings just as it has through much of 2021 but now we have reporting season thrown into the mix and its driving a performance wedge across the market – the price action on Thursday felt like 2 totally different markets running their own race, as opposed to a number of individual names within the ASX200 e.g. 10 stocks rallied by over 4% while 9 names fell by the same degree. The important thing to remember is how quickly sentiments changing in todays fickle environment with Commonwealth Bank (CBA) and BHP Group (BHP) both making fresh all-time highs in recent weeks currently being thrown unceremoniously into the naughty corner which suggests to MM they can easily return to grace just as fast.

The COVID numbers might appear dreadful on the surface but the vaccination rates are soaring with over 55% of NSW having already received their first jab, unfortunately the dramatic spike in cases & lockdowns has been the required catalyst to get people into the clinics, chemists etc. Economic optimism has fallen off the proverbial cliff since June with Australian 10-year bond yields almost halving from their high in Q1, but if we look 3-6 months out the re-opening trade Mark 2 is likely to be back in full swing – we feel pessimism is now getting ahead of itself focusing on today as opposed to the likely scenario closer to Christmas hence MM is considering ways to migrate up the risk curve across our portfolios.

Overnight US stocks recovered from deep early losses to close mixed in a volatile session where big tech dragged the market higher. Bond yields, commodities and the Aussie fell leading to further losses in the US Resources Sector with the big question being asked “can the global economy absorb the reduction of stimulus in the face of the persistent spread of COVID and slowing Chinese growth – another example of the obvious hurdles being ignored for months before everyone hits the exit doors all at once.

The SPI Futures are calling the ASX200 to recover yesterday’s losses even with BHP Group (BHP) poised to open down another 2% this morning.

MM remains a buyer of weakness across most stock market sectors

Add To Hit List