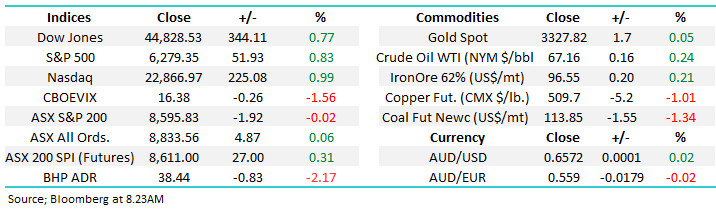

- What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

On Tuesday, the ASX200 delivered a perfect example of how investing is far more about stock/sector performance than the underlying index, which attracts too much attention. So far, 2024 has been dominated by interest rate-sensitive stocks, with the Tech, Financials and Real Estate sectors all up over +20%. Conversely, the materials and energy names were down over 15% before yesterday’s dramatic reversion – one day doesn’t make a summer, but it did catch our attention:

- The PBOC announced that China will reduce the reserve requirement ratio or the amount of cash banks must hold by 0.50%, freeing up liquidity across the financial system and sending bond yields to a record low.

- The PBOC also announced a cut in existing mortgage rates and indicated that a 0.2-0.25% reduction in the loan prime rate was on the table, though they did not clarify when this might happen.

- PBOC Governor Pan Gongsheng also announced at least 500 billion yuan of liquidity support for stocks and that new measures to encourage M&A will follow soon.

The sudden high-level press conference was announced on Monday following last week’s outsized interest rate cut by the Fed, and the PBOC announcement initially smacked of whatever you can do; we can do better, with their aggressive stimulus being more than most pundits expected. However, the much anticipated Fed pivot may allow China’s central bank to lower its rates further to stimulate growth as a property crisis adds to increasing deflationary pressures. The initial reaction by equities was bullish, with China and Hong Kong markets surging by over 4%. On the ASX, the gains were even more dramatic in China facing resource names:

- Mineral Resources (MIN) +7.1%, Sandfire Resources (SFR) +6.2%, Whitehaven Coal (WHC) +6.1%, Iluka (ILU) +5.8%, South32 (S32) +4.1%, RIO Tinto (RIO) +3.7%, Lynas (LYC) +3.7%, and BHP Group (BHP) +3.3%.

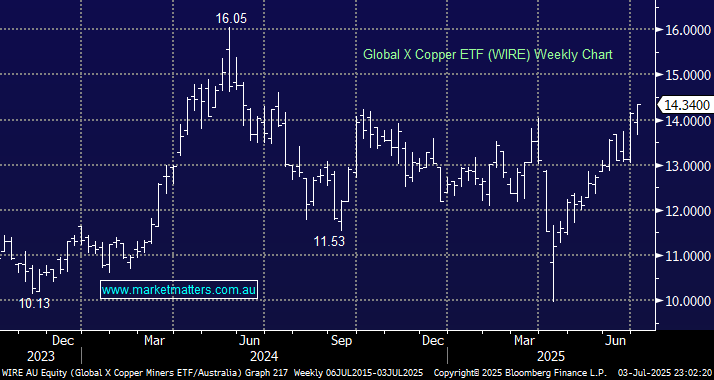

Follow-through looks likely this morning, with Copper Futures extending initial gains during our day session to close up more than 4% in the US, helping Cu ETFs advance over 7%. The $A surged towards 69c, testing 12-month highs, suggesting markets give China’s strong stimulus measures a reasonable chance of success. Gold also closed up another +1.3%, pushing related ETFs up over +2.5%, pointing to a strong session today across most of the Materials Sector.

Overseas equities were firm overnight; the EURO STOXX 50 and French CAC closed up over 1%, while the UK FTSE only advanced +0.3% as Prime Minister Starmer attempts to tighten the country’s financial belt. The US S&P500 rose for a second consecutive day to a fresh record on Tuesday, dismissing a weak consumer confidence print. Not surprisingly, dual-listed China stocks stood out Tuesday following Beijing’s stimulus efforts to stoke economic growth. U.S.-listed shares of Alibaba (BABA US) and JD.com (JD US) climbed 7.9% and 13.9%, respectively while China large-cap ETFs were up ~10%.

- This morning, the SPI Futures are pointing to a +0.3% gain early this morning, with BHP Group (BHP) closing up another ~1% in overseas trade.

MM is neutral toward the ASX200

Add To Hit List