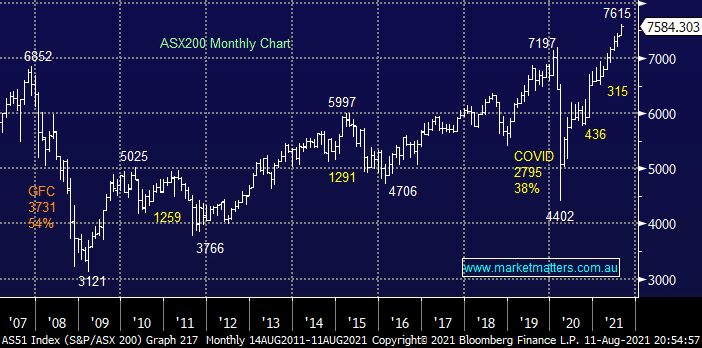

The ASX200 continues to grind higher, we might often be closing well under the intra-day high but before we know it the index has again pushed through to post new all-time highs. On a day to day perspective this rally feels slow and steady, almost like 3 steps forward and 2 back, but when you stand back and look at the monthly chart of the local market its resembling a vertical line which could easily defy the bears and test 8,000 in the next 6-months – remember a stock market which ignores bad news is strong and an economy enduring repetitive lockdowns is certainly not providing the best backdrop for corporate growth & certainty e.g. Consumer confidence has fallen to its lowest level this year but note it still remains well above the lows of 2020 when we hadn’t even discovered a vaccine.

Wednesday was primarily a Commonwealth Bank (CBA) party as Australia’s largest listed company reported strongly for the year helping the stock rally +1.5% to fresh highs, contributing almost half of the markets 22-point gain in the process. Reporting season and rising bond yields have provided a strong tailwind for the banks although we can see them enter a period of consolidation in the near future as the latest news sugar hit slowly becomes absorbed by the market. However if the ASX follows in the same mode of the last 6-months another sector / theme will take on the performance baton, perhaps we will see some more high profile M&A, whatever the outcome the noticeable absence of selling has been the dominant characteristic of this market’s advance post the coronavirus outbreak.

Wednesday was regarded by many as D-Day for US inflation and the relatively muted numbers helped bonds rise / yields fall as concerns around the need to ease stimulus faded. The CPI came in at 0.5% compared to 0.9% in June which when combined with ongoing strong demand for US bonds during an auction overnight reversed slightly the latest rally by US bond yields. At this stage the Feds September taper announcement is far from a “done deal” as COVID numbers continue to increase courtesy of the Delta Strain, a few more months of economic data feels necessary to clarify if the recent pick up in inflation is here to stay but bonds will undoubtedly lead the data i.e. follow the money flow.

Overnight US equities experienced another mixed session with the Dow rallying +0.6% to fresh highs while the tech based NASDAQ slipped -0.2%. The rotation to cyclical names from the FAANG’s et al is slowly gathering momentum and at MM we still believe its early days for this rotation. The SPI Futures are calling the ASX to open slightly higher today helped by a 30c rally in BHP Group (BHP). Under the hood the S&P500 saw Financials and Resources continue to outperform aided by the declining $US which boosted the likes of gold and crude oil.

MM remains a buyer of weakness across most stock market sectors

Add To Hit List