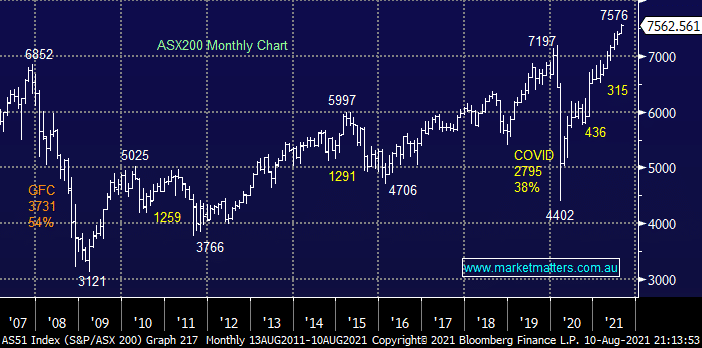

The ASX200 again posted new all-time highs yesterday, local stocks continue to march ever higher with IT and Banking the backbone of the Tuesdays +0.3% gain. The local market continues to follow the rhythm of the rally which commenced back in February, we’ve now seen the local market appreciate over 1000-points / 16% in just 7-months with our target for this August ~7650 but until further notice the most important factor to remember is the bulls are in control and cash is most definitely not king. We believe the key to adding value until 2022 is stay core long and choose the correct stocks / sectors to hold very carefully.

One of the main contributing factors to the recent surge in equities this year has been fund managers moving out of bonds as yields have tumbled e.g. since February US 10-year yields have fallen from 1.77% to 1.13%, the exact same period over which the ASX has punched 16% higher. Firstly let’s consider some of the highlights of last month’s closely scrutinized Bank of America Fund Managers survey:

- Most fund managers believe the economy has reached “peak boom” as concerns grow around growth, earnings and inflation i.e. economic growth expectations are at 47%, down from the 91% peak in March.

- They have a bias towards cyclicals with investments in commodities reaching a record high – as we alluded to in yesterday’s report there is plenty of support into pullbacks for the local resources stocks.

- US rates aren’t now expected to rise until the 2nd half of 2022 with the Delta Variant likely to push this back even further, probably into 2023.

- Fund managers regard Tech followed by ESG assets and then Bitcoin as the most crowded trades.

NB ESG-focussed assets are those which follow environmental, social and corporate governance e.g. clean energy as opposed to fossil fuels.

Secondly and arguably most importantly cash balances have increased from 3.9% to 4.1% with 58% of fund managers now overweight equities while 68% are underweight bonds – remember global bond markets are significantly larger than equities hence a few % pushed up the “risk curve” into stocks in search of better returns has a meaningful impact on equities indices.

At MM we are bullish stocks but clearly so are many other professionals hence we still expect a minor washout style ~5% pullback at some stage in coming months but again its one we want to buy. The catalyst for such a dip is likely to be an ongoing rally in bond yields and subsequent tweaking by fund managers back towards bonds, from overweight stock positions.

Overnight we saw another mixed session by US stocks with a strong session by Financials and Resources but weak performances from growth and yield sensitive areas as bond yields continued to rally. MM anticipates this outperformance by the likes of banks & resources compared to Tech and Healthcare has further to unfold as the former plays some catch-up.

MM remains bullish the ASX and keen buyers of pullbacks

Add To Hit List