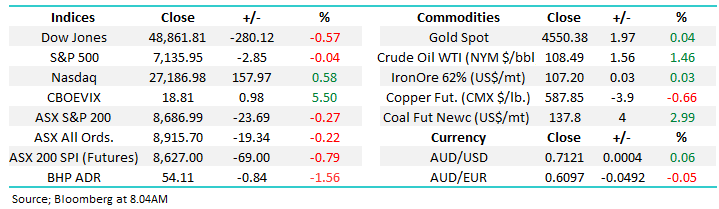

The ASX200 tried hard to rally yesterday but the selling across the “re-opening trade” and Resources Sector offset the strength in the Banking Sector, pretty much in line with our expectations flagged in yesterday’s report. MM has been bullish the banks for months and yesterday saw the Insurance Sector join the “rising bond yield” party, we like both the Banking & Insurance Sectors at this stage of the bond yield cycle although our medium-term target for Commonwealth Bank (CBA) is now only 5% away as we approach their report on Wednesday, hopes are clearly high on the dividend / buyback front.

As mentioned the resources stocks struggled on Monday but overall we felt they were resilient considering the rising $US and falling commodity prices e.g. Newcrest Mining (NCM) only fell -2.7% yet gold collapsed $US85/oz early in the morning, it felt like traders had analysed the US Employment Data over the weekend and decided the Greenback & bond yields were going up hence there was no reason to own commodities, or resources stocks. However even with copper down a relatively subdued -1.5% we saw OZ Minerals (OZL) actually close up on the day in a clear sign that MM is not the only player looking to accumulate weakness across the sector.

M&A again raised its head yesterday although on a less public level than with Afterpay (APT), last week Tasmanian salmon producer Huon (HUO) received a $3.85 takeover bid from Brazilian meat giant JBS. The original $550m bid was at an almost 40% premium to its previous close signalling a very serious approach but interestingly on Monday we saw 10% of the company’s shares exchange hands at the $3.85 bid price. Iron ore magnate Andrew “Twiggy” Forrest who already owns 7% of HUO is rumoured to be the buyer, things might just be getting interesting down in Tasmania. The key takeout for MM is we may have seen a few bids withdrawn of late but we believe corporate activity is alive and well and the next few takeovers may get trumped as opposed to withdrawn, it’s what often happens in bull markets.

Overnight US equities were mixed in a reverse of Fridays move with the Dow falling while the NASDAQ rallied although overall it was a quiet session that seemed to take some solace from the lack of follow through by the $US / bond yields on the upside and commodities down. The SPI futures are calling the ASX200 to test yesterdays highs early this morning, up around 30-points helped by a 1% bounce by BHP Group (BHP).

MM remains a buyer of weakness across most stock market sectors

Add To Hit List