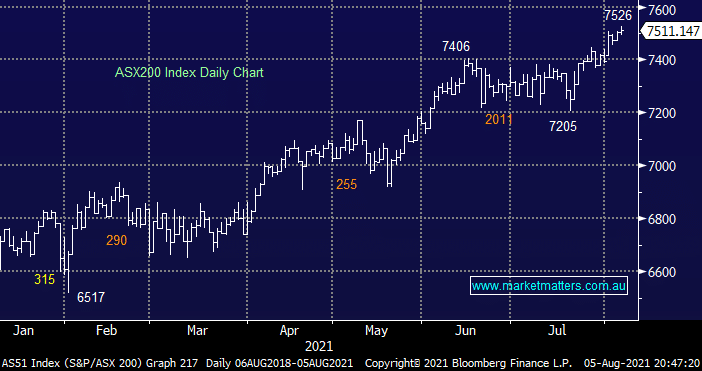

Thursday delivered a steady session for the ASX200 which finally closed at another new all-time high although it didn’t feel like that sort of day with no stocks moving in either direction by more than 3.5%. If we were to try and dissect the meagre +0.1% advance it would be a case of gains by the Banks and Real Estate stocks was more than enough to offset losses in the Resources names. The market feels like it’s slowly starting to accept the new 7500 handle just as it did 7200-7400 and 6900-7100 trading ranges earlier in the year.

The global impact over recent weeks of the Delta Strain has caused an understandable shift away from stocks / sectors dependant on economic expansion into perceived areas of safety such as the supermarkets e.g. Woolworths (WOW), Coles (COL) and Metcash (MTS) have all outperformed over the last month. As we said the “recovery stocks” have struggled but we feel their relative demise has been exacerbated because it became the crowded / obvious place to be overweight as most investors believed the coronavirus was in the rear view. The next twist in this tail feels harder to call especially if we look back in history which warns us future waves can be far worse, fortunately we are so lucky that medical science have delivered effective vaccines.

Interestingly overnight as the majority of Asia struggles with the virulent Delta Strain prominent US investment bank Goldman Sachs (GS US) came out and upgraded their forecast for the S&P500 Index due to higher than expected earnings growth and lower than anticipated interest rates. Their target for the end of 2021 is now 4700 targeting another 7% upside over the coming 4-months, not bad considering the excellent gains year to-date – this is now the highest forecast on Wall Street but I wouldn’t be surprised to see a few others follow suit. They believe corporates and retail investors are the likely major buyers due to buybacks and large cash holdings but as a cautionary note they are only looking for 4900 by the end of 2022, with bond yields becoming an eventual concern.

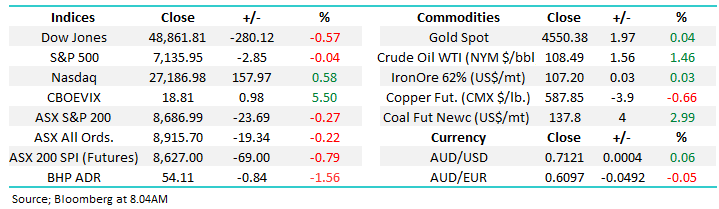

Overnight US equities rallied ahead of tonight’s employment report, solid earnings are certainly winning the arm wrestle with COVID as strength across most sectors saw the indices gain another ~0.6%. The SPI Futures ignored the overseas strength signalling a flat open by the ASX not helped by BHP Group (BHP) falling more than a $1 in the US.

MM remains a buyer of weakness across most stock market sectors

Add To Hit List