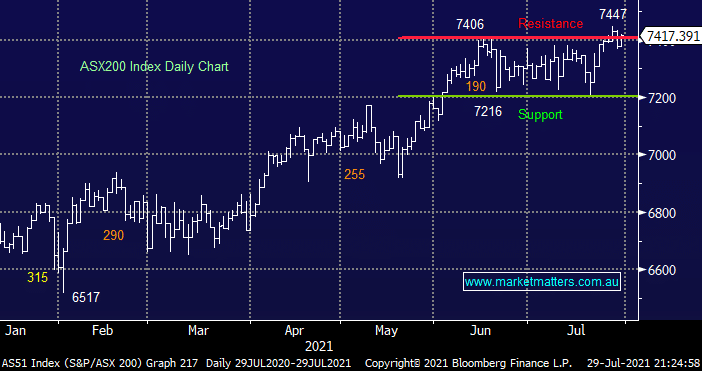

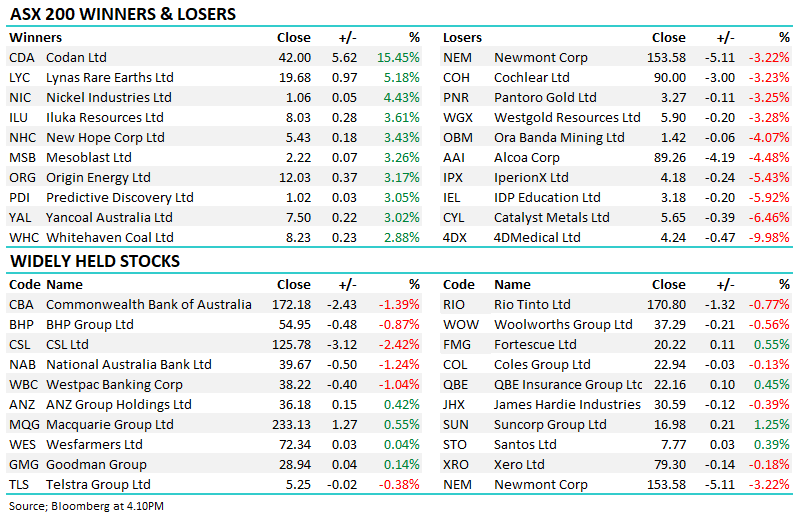

The ASX200 performed another 180 degree pirouette yesterday, one which was almost good enough for the Tokyo Games! The market continues to remind me of a washing machine spinning stocks and sectors in almost random direction with the underlying upside bias the only constant. The Tech stocks were best on ground yesterday after struggling on Wednesday, every stock in the sector rallied led by takeover target IRESS (IRE) which received a higher offer from EQT although interestingly the stock still closed ~8% below the bid as boards continue to reject most approaches which cross their desks. Elsewhere the iron ore stocks punched higher after RIO Tinto’s (RIO) strong report, all of the “Big 3” we covered yesterday closed up over +1.5% also registering fresh all-time highs during the day.

Australian bond yields continue to drift lower as the Sydney COVID outbreak feels like its spiralling out of control, the army are now poised to patrol the streets, to someone living in Sydney its shocking how badly things have escalated since one limo-driver passed on the virus only in mid-June. This continuation lower by yields is having a mixed influence on stocks / sectors as our call in January for a bullish but choppy / rotational style year remains on point although unfortunately often for the wrong reasons. However over the last 3-months some of the correlations in Australia aren’t what we would normally expect considering the macro backdrop:

- Bond yields falling has halted the strong advance by the banks, with the exception of Commonwealth Bank (CBA) – this makes sense.

- The re-opening trade has been hit hard as travel and holidays now feel like a dream to so many of us – again this makes sense.

- The Healthcare stocks have performed reasonably well while IT have struggled, usually we would expect both sectors to embrace lower yields, as they have in the US.

- As 25,000 Sydneysiders currently lose their jobs every week the Retail Sector remains strong, it might be right but the risk / reward concerns MM.

- The Utilities / “yield Play” stocks don’t appear to believe that the lower yields will be around that long i.e. they’ve struggled outside of takeover offers.

- The Resources Sector is back in vogue, outperforming their underlying commodities and ignoring global bond yields calling a global economic slowdown.

We believe until a new trend emerges investors need to avoid getting caught up in the volatile short-term whipsaws of the market, it’s good for brokers but not investors. MM has recently tweaked our portfolio away from IT towards the Resources, while maintaining a reasonable cash level to take advantage of any opportunities which may present themselves – we remain happy with the stance at this point in time.

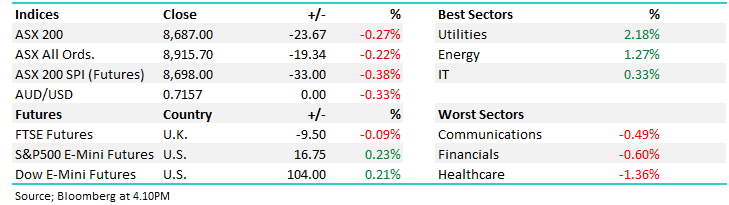

Overnight US stocks again pushed higher to new all-time highs with GDP data (growth) coming in below expectations reducing inflation fears in the process, Financial & Material Sectors were the best on ground which would usually support the ASX although the futures are pointing to an unchanged open this morning – BHP Group (BHP) is set to open at fresh highs, up over $1 well above $54.

MM remains a keen buyer of stocks into pullbacks

Add To Hit List