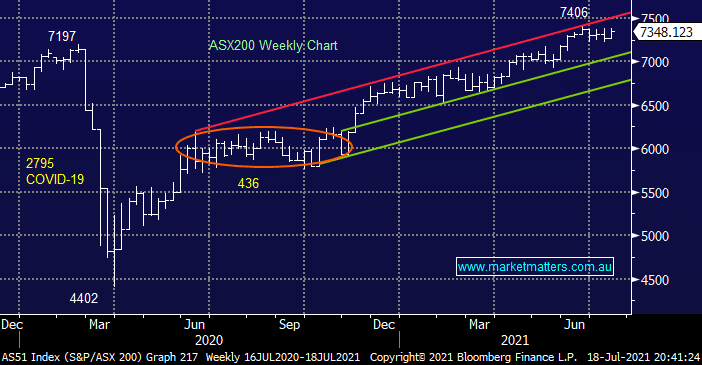

The ASX200 continues to trade sideways in the face of a deteriorating COVID picture although it hasn’t actually been going anywhere since early June, well before the current Delta wave raised its head on our fair shores. Sydney registered its first case of this outbreak only 30-days ago on the 16th of June, it already feels a lot longer in the Gerrish household! As the the State and Federal Governments again dig deep to support individuals and businesses unable to work due to lockdowns optimism towards the speed of the economic recovery has waned but on the stock market level it’s only produced some rotation between sectors as opposed to core market selling.

- The Australian 10-year Bond Yield has fallen from 1.93% to 1.28% since late February, perhaps banks will again start cutting 3 & 4-year fixed mortgage rates back under 2%.

- The $A which is often used as a proxy for future economic strength has fallen from 80c to 74c, again since late February.

Basically confidence towards both the local and global post pandemic economic recovery has been slipping for well over 4-months and the current increasing COVID cases across the globe from Japan, to the US plus of course the UK has surprisingly had no impact on equities, they continue to almost embrace the economic backdrop of declining bond yields as they maintain a positive glass half full attitude. The underlying feeling to MM is one of classic “FOMO” but in this instance its not a case of missing out on say the charge higher in lithium or BNPL stocks but this time it’s the market in general:

- It feels like fund managers / investors are scared to sell / or move underweight equities after witnessing how stocks rallied from March 2020 thanks to unprecedented stimulus.

MM remains happy buyer of weakness over the coming weeks with an ideal target for the index ~7,000

Add To Hit List