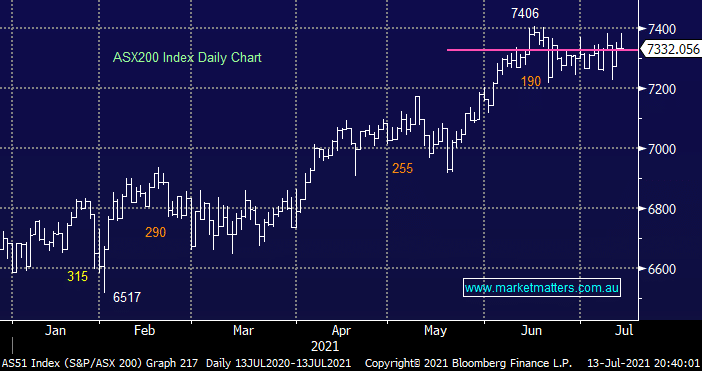

The ASX200 again succumb to the almost magnetic pull of the 7300 level, the index has been rotating around this area within +/- 100-points for over a month but from my perspective it feels even longer! Yesterday saw the market forgo early strong gains to close basically unchanged with the Banking, Energy and Real Estate Sectors weighing on the ASX but the selling was very restrained with only 1 stock falling by over 3% i.e. no change, there are buyers of weakness and sellers of strength but neither appears particularly committed to their cause.

Elsewhere in Asia the mood was far more buoyant as stocks embraced the significant fresh economic stimulus delivered by the PBOC on Friday, potentially the domestic COVID issues may be dampening the ASX’s mood with local bond yields drifting lower as the Sydney lockdown casts a shadow of doubt over the speed of our economic expansion for the coming 6-12 months. We feel investors have swung from being way too optimistic in February to now testing the pessimism side of the coin – more on this later.

MM’s positive medium-term outlook towards the “reflation trade” is borne from 2 simple pieces of recent history:

- Central banks have proven on a number of occasions that they will do “whatever it takes” to maintain economic growth and we know they can keep printing money even if COVID does create another major bump in the road.

- When China presses the stimulus button it’s not prudent to be caught in the way as they continue on their quest to become the world’s largest economic powerhouse.

MM remains a keen buyer of market dips with the 7000 area the first technical support area

Add To Hit List

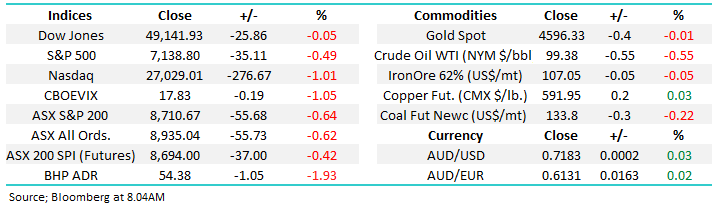

Overnight US stocks drifted -0.35% with the exception of the tech sector which closed unchanged, the SPI futures are calling the local market to open basically flat this morning although BHP looks set to regain yesterday’s losses early on in the session.