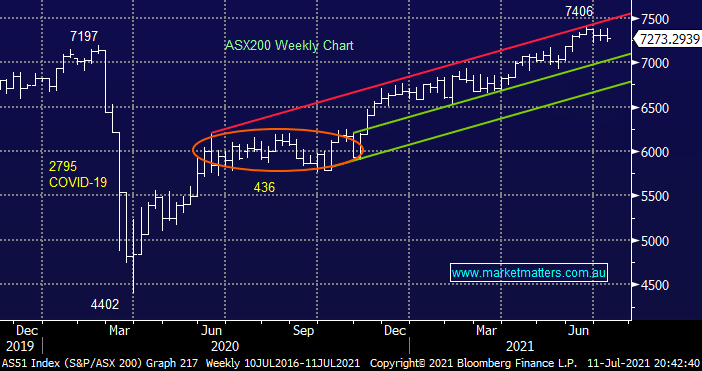

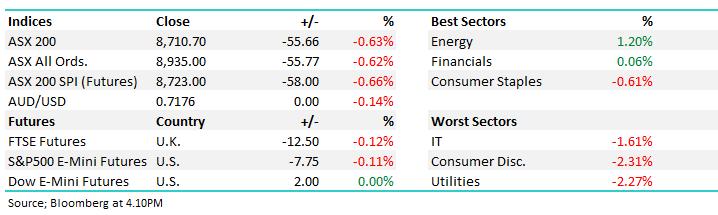

The ASX200 continues to bounce around between 7200 and 7400 which considering the economic and social backdrop is an impressive performance in my opinion. The local index has rallied ~28% over the last 9-months yet the very real prospect of a damaging extended lockdown in NSW is being shrugged off by stocks, although both bond and currency markets are taking more notice:

- The Australian 10-year bond yield has now fallen from 1.93% to 1.32% over recent months as faith in the post COVID economic recovery wanes.

- Over a similar period the $A has fallen from 80c to sub 75c, underperforming virtually all global currencies along the way.

NB Due to our hefty dependence on commodities such as iron ore and copper the $A is often used as an indicator of future local and global economic strength.

Investors have remained committed to risk assets, the index remains within a few percent of its June all-time high but while they’ve had no interest in pulling money from stocks there has been a significant change of heart as to which sectors are best positioned as the economic recovery takes a new twist. The rotation is very easy to comprehend as bets have shifted away from the reflation trade i.e. Broadly speaking the Tech & Healthcare stocks has been outperforming the Resources & Financials. However adding value is about looking through the windscreen as opposed to the rear view mirror, we are considering 2 simple questions today.

- Can risks assets maintain their resilience in the face of a deteriorating COVID picture, especially in Sydney – stocks appear to be priced for a recovery not a lacklustre economy.

- Has the rotation from value to growth stocks got further to go i.e. are bond yields approaching a low.

By definition any ongoing conclusions around the above 2 scenarios will dictate how and when MM tweaks portfolios over the coming weeks / month but we do remain a buyer of dips by stocks.

MM remains a happy buyer of weakness over the coming weeks with an initial target for the index ~7,000

Add To Hit List