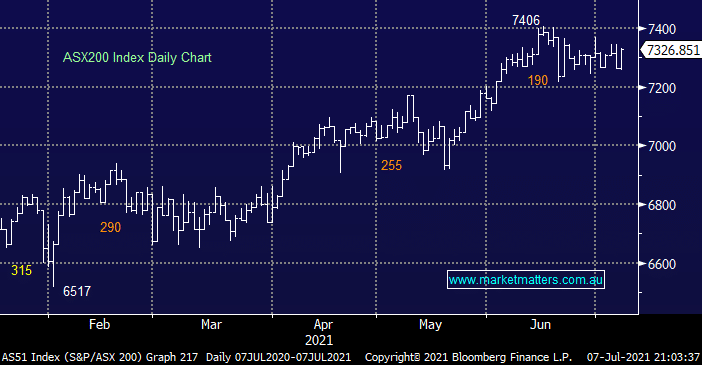

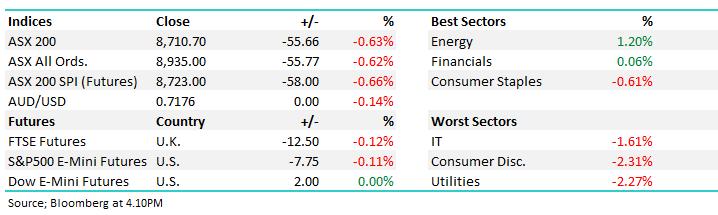

Yesterday saw the local market rally +0.9% more than recovering the losses on Tuesday, the growth names led the line following US indices overnight who embraced the drift in US bond yields i.e. Tech & Healthcare. The stock and sector rotation continues while the ASX200 remains basically unchanged since the start of June, below are some of the names catching our eye for both good and bad reasons:

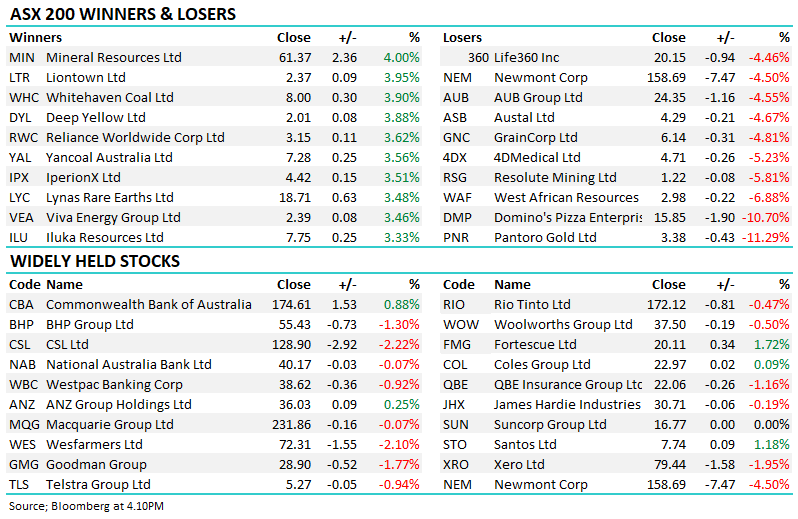

Winners : Zip Co (Z1P) +12.2%, Challenger (CGF) +10%, Whitehaven Coal (WHC) +15.8%, a2 Milk (A2M) +21.8%, ResMed (RMD) +24%, carsales.com (CAR) +12%, Afterpay (APT) +24.5% and TPG Telecom (TPG) 15.3%.

Losers : Westpac (WBC) -3.9%, Crown Resorts (CWN) -9.1%, Santos (STO) -6.8%, OZ Minerals (OZL) -13.4%, Alumina (AWC)-7.8%, Lend Lease (LLC) -10.3% and AGL Ltd (AGL) -10.2%.

One thing that popped out at me when I assessed the stocks over the last month was the mean reversion that’s becoming ever more commonplace i.e. profit talking is hitting some top performers while bargain hunting is gathering momentum. We’ve said a number of times that 2021 will often be about selling strength and buying weakness and there’s no reason to believe the next 6-months will be any different.

If I was to briefly summarise the look and feel at the moment it would be the index is a coin toss but there’s plenty of buying into weakness, the banks feel tired after their strong gains in 2021, Energy stocks are cheap but feel capable of underperforming further, Healthcare stocks are embracing the drift in longer dated bond yields but not as much as Tech, gold stocks feel cheap but the $US is a headwind short-term, most of the resources are in no mans land but the $US is again an issue and lastly M&A remains an important game in town as large war chests of cash scour the landscape for opportunities.

Overnight US stocks again eked out gains with the S&P500 rallying +0.3% to fresh all-time highs, the SPI futures are calling the local index up +0.2% with BHP set to open up 65c.

MM remains a very keen buyer of stocks into pullbacks

Add To Hit List