The ASX200 rallied strongly yesterday to close up 1.1% with over 80% of the market closing up on the day, if it hadn’t been for some profit taking in the energy & mining stocks it would have undoubtedly been a rare triple digit gain for the local index. Much of the strength flowed down from a pullback in oil prices following comments from the Ukraine that’s it’s open to peace talks with Russia, travel stocks were not surprisingly the standout winners e.g. Qantas (QAN) +5.8%, Webjet (WEB) +5.8% & Fight Centre (FLT) +6.6%.

- MM believes the Resources Sector is looking for / close to a top but considering the geopolitical tensions surrounding Ukraine they could easily again test the upside over the coming weeks.

The influential Banking Sector made up well over 40% of the markets gain on Thursday with the Big Fours average gain almost 3%, significantly outperforming the market in the process – more on this later. The Diversified Financials also rallied strongly with all 15 stocks in the sector closing up on the day but interesting all 15 are down year to date with almost half down by 20% or more – remember yesterday morning we said– “if MM is correct we should be poised to see some major reversion on the performance front that has played our over the last few months”.

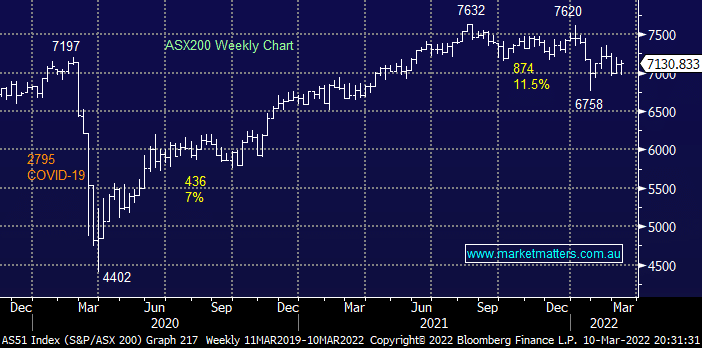

It feels like stocks have been on a crazy news induced volatility ride over recent months but the index is actually basically unchanged over the last 12-months, all the action remains on the stock & sector level. Bond yields have dominated proceedings since the Australian 3-year yield started edging up from 0.1% this time last year to reach fresh 3-year highs at 1.778% yesterday, a cocktail of rising inflation and a strong post COVID economic recovery has fuelled fears that central banks will start aggressively hiking interest rates sooner rather than later.

- MM believes interest rates are set to rise but we feel bond yields have rallied too far, too fast, considering the potential fallouts from the Ukraine and lag on expansion due to COVID / supply chain disruptions.

Overnight we saw US stocks fall after the US registered its highest inflation reading in 40-years sending bond yields higher and tech stocks down in sympathy. The SPI futures are calling the ASX200 to open down 0.50% with value stocks looking set to outperform growth names as in financial markets bond yields take back the limelight from the Ukraine invasion.

MM remains neutral to bullish the ASX while its below 7200

Add To Hit List