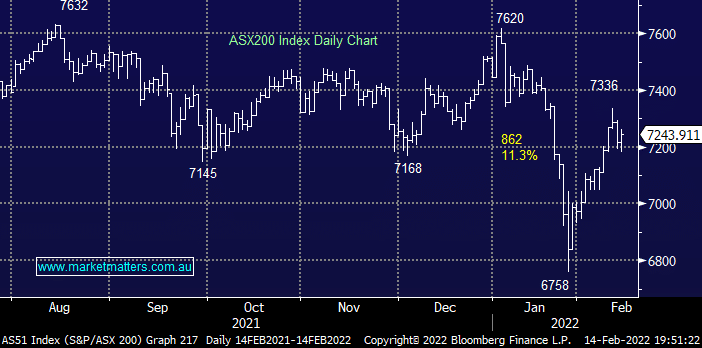

The ASX200 put in another solid performance yesterday to start off the week by ignoring Fridays 500-point plunge by the Dow to close up an impressive 0.4%, as we’ve said previously the more time the index can consolidate above 7200 the higher our conviction becomes that it can test 7600 in the coming months. However yesterday’s buying wasn’t broad based with only 42% of the index closing in positive territory but when the banks are extremely strong it usually translates to gains in the index e.g. Westpac (WBC) rallied +4.8%. We feel like the ASX wants to rally but overseas jitters around both the Ukraine and inflation are far from over, after recovering over 65% of the early 2022 losses it currently feels a big ask to expect stocks to extend their gains before they at least take a rest and / or the macro back drop improves.

The strength locally on Monday was even more impressive when we consider other moves across the region with Asia and even NZ falling fairly hard e.g. New Zealand -1.8%, Japan’s Nikkei -2.2% and South Koreas KOSPI -1.6%. However until we can see some strength aside from the banks its unfortunately highly unlikely the Australian market can push significantly higher but as an optimist I find myself thinking “how hard could we rally if Mr Putin put down his sabre and we saw a few relatively benign inflation numbers over the coming months?”.

Aside from the banks both the oil and gold stocks were strong on Monday with the former maintaining recent strength while precious metals dominated the winners enclosure for the 1st time in months. Bond yields fell as expected after the moves in the US on Friday but it wasn’t enough to translate into any meaningful buying in tech stocks which continue to feel entrenched in the belief that growth stocks will fall as inevitable interest rate hikes roll across the globe in 2022/3 – we remain very conscious of this very one-sided opinion on sector performance through 2022.

Overnight saw European stocks plunge over 2% on geopolitical concerns around neighbouring Ukraine but US indices staged a solid comeback after dipping fairly hard early in the session with tech stocks finally enjoying some buying into weakness. Unfortunately the SPI futures are calling the ASX to follow Europe, as it usually does, and drop nearly 1% early this morning with BHP Group (BHP) trading down around 1% in the US.

MM remains bullish the ASX while its above 7200

Add To Hit List