The ASX200 put in a solid result yesterday managing to close slightly higher even after a torrid session on Wall Street, only 30% of the index closed positive but the gains in the resources names were enough to tip the balance. Gold stocks were the undoubted standouts across the board with even the relatively conservative play Newcrest Mining (NCM) managing to surge over 6.5% while our other specific exposure to the sector in MM’s Growth Portfolio, Northern Star Resources (NST), was the main boards top performer surging over 11% on the day.

Chinese banks have cut borrowing costs as the PBOC eases and talks a dovish game, on Wednesday night comments from affiliated state media spouted rhetoric along the lines of “China has now opened its monetary policy toolbox and won’t allow growth to drop below 5%” these comments have certainly helped commodities firm further. It is important to remember that when Chinese authorities set targets, they rarely miss them – good news for both the $A and Resources Sector in general.

- Remember MM is looking for a “pop” high in commodities and the related stocks this quarter of 2022, this could easily prove the catalyst..

Bond markets have quietened slightly over the last 24-hours which was enough to see Asian tech start to enjoy a bid tone and US names try and bounce albeit unsuccessfully overnight however there are clearly plenty of jitters still in the sector. Interestingly overnight Macquarie Bank made some fairly dovish comments around interest rates putting them in the same camp as our good selves i.e. they don’t believe central banks will abandon their low interest rate mandates in too much of a hurry. Similar to MM they feel that the current kick in inflation is largely linked to supply chain constrains and hence on balance largely transitory in nature.

- Markets are currently looking for a hike by the RBA in June and 3 or 4 hikes by the Fed throughout the year.

Overnight we saw Wall Street attempt to recover before tech stocks tumbled into the close with the NASDAQ finally reversing gains of 1% to close 1.3% lower. The SPI futures are pointing to 1% lower open this morning after the volatile and largely bearish night & week, BHP didn’t help overnight slipping around 1% lower in US trade as the unification vote got up in the UK.

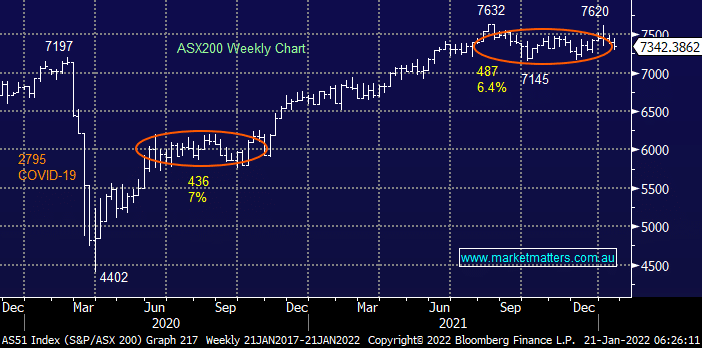

MM remains bullish the ASX targeting fresh highs in 2022

Add To Hit List