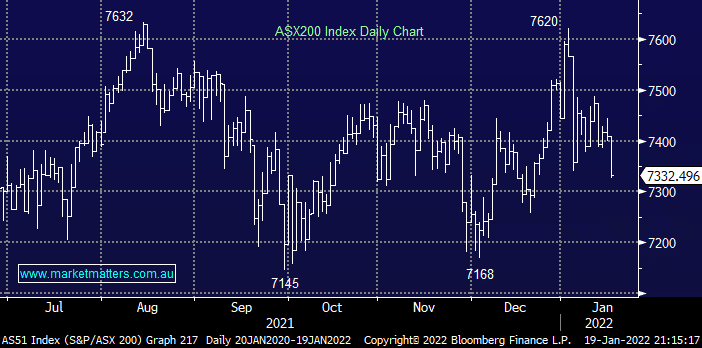

Yesterday felt like “15-love” to bond yields as the ASX200 was clobbered 76-points following a bad session on Wall Street which was then compounded by further weakness in the S&P500 futures during our day session. However 25% of stocks did still manage to close up on Wednesday with the gains feeling far more stock specific as opposed to switching between sectors which has been the main story over recent months e.g. within the topical IT Sector Appen (APX) rallied 3.9% while Wisetech (WTC) fell 3.8%.

Rising bond yields also pressured most equities across Asia but it was in the engine room of credit markets themselves where the moves were the most pronounced, if the strength of the last few weeks is maintained by domestic bond yields I would expect another tweak higher in home mortgages before we enter February. To add fuel to the inflation fire overnight the UK saw its CPI surge to 5.4%, economists were expecting a 5.2% print, this surprise increase took UK inflation to a 30-year high exerting more pressure on the Bank of England to hike rates further following on the coattails of the lift in December from 0.1% to 0.25%.

- MM is certainly seeing all the ingredients for our targeted panic spike higher in global bond yields.

Historically fund managers don’t make a full return to work until after Australia Day hence some stock allocation is likely to commence in earnest after next Wednesday, hence if stocks are still drifting lower into the middle of next week an inflection point would become our preferred scenario – how long it lasts would become key. Similarly US equities should find some support come Friday as the “blackout period” for company buybacks is lifted i.e. US companies cannot buy their own stock into reporting season which removes a major tailwind of the last few years.

Overnight we saw a choppy and volatile session on Wall Street with tech stocks attempting to bounce but ultimately failing with the broad based S&P500 closing down 1%. The SPI futures are calling the ASX200 to open mildly higher this morning helped by a strong session looking on the cards for the Resources Sector e.g. BHP Group (BHP) is trading around 2% higher in the US.

MM remains bullish the ASX targeting fresh highs in 2022

Add To Hit List