The ASX200 enjoyed a solid Thursday courtesy of ongoing strength in banks and resources with heavyweights BHP Group (BHP) & RIO Tinto (RIO) both gaining around 4%. Losers marginally trumped the winners but when the indexes 2 largest sectors, which make up around 40% of the market rally the index tends to follow suit. Blackstone’s increased bid for Crown Resorts (CWN) also helped market sentiment as it demonstrated that M&A remains alive and well for undervalued assets arguably creating a bid into any decent sell-offs in risk assets.

We believe the market continues to exhibit a bullish “look & feel” as it ignores Omicron numbers and major supply chain disruptions which is now being hugely exacerbated by staff issues as the virus spreads throughout NSW, VIC and QLD e.g. I went into a bank yesterday and commented to the teller that I was surprised how busy they were, I was informed that the closest 3 branches were all closed due to COVID infections making them the only option within miles i.e. these issues look destined to remain for a few weeks but with hospitalisation rates only nudging higher the market clearly remains optimistic that the country will not again close for business, only mildly inconvenienced – we agree with this interpretation at MM.

Volumes remain seasonally light as people return from extended vacations, even the U.S. inflation print hitting a 39-year high hasn’t injected much urgency into proceedings with the only move of note being a fall by the $US i.e. markets were clearly positioned for the largest 12-month gain by the CPI since 1982. When we combine rising inflation with US employment falling under 4% the likelihood of 4-5 rate hikes this year feels a given but again markets are taking this in their stride for now while they start to 2nd guess what comes next later in 2022, and beyond.

Overnight saw a choppy session on Wall Street which closed near the session lows, the Dow fell 0.5% while the tech stocks plunged over 2.5% as selling returned to the growth sector, interestingly ignoring bond yields drifting lower – Tesla (TSLA US) and Microsoft (MSFT US) were two of the major losers falling over 4% and 6% respectively. The SPI futures are calling the ASX200 to dip 0.5% early on this sunny Friday morning in Sydney

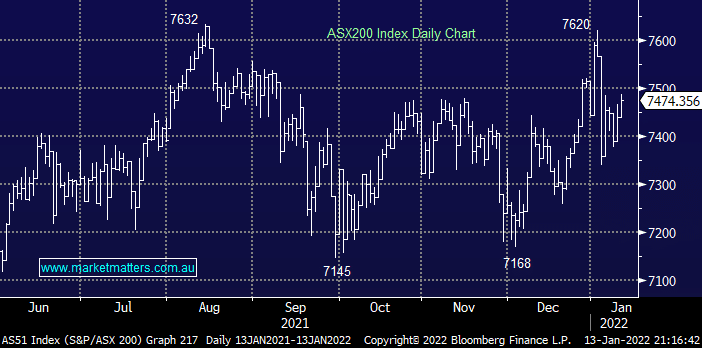

MM remains bullish the ASX targeting fresh highs in 2022

Add To Hit List