The ASX200 fought valiantly on Monday to only slip 11-points considering Magellan (MFG) tumbled over 30% and US futures literally melted before our eyes on the combination of intensifying Omicron fears and diminishing confidence in Joe Bidens ability to drive US economic expansion. Interestingly while falls reverberated across major global equity markets Australia and New Zealand held firm with the later actually managing to rally 0.38%. Overall it was a confusing day where the more one tried to make rhyme or reason of the swings the more conflicting things became, the only consistent was buyers emerged into morning weakness almost taking the market into positive territory by the close i.e. the same tale we’ve witnesses through most of 2021.

- Omicron was blamed for much of the aggressive selling in the US S&P500 futures yet in the ASX the majority of the recovery names closed up on the day.

- Oil stocks fell on global economic worries yet copper names such as OZ Minerals (OZL) remain close to their multi-year highs.

- Bond yields only edged lower indicating they are far from convinced that the Omicron strain and Joe Bidens woes are going to derail economic expansion.

Our feeling is short term traders had got themselves long US futures looking for a “Christmas Rally” but the markets become understandably nervous around current elevated market valuations in the face of rising global case counts making the short-term path of least resistance suddenly down. Conversely the ASX which hasn’t participated in the 13% advance by the S&P500 over the last 6-months, posting fresh all-time highs along the way, hence Australian stocks are far more resilient to these sharp spikes to the downside because we don’t have a pool of traders being stopped out of long positions.

We also finally saw China give the ASX a helping hand as Chinese banks lowered borrowing costs for the first time in 20-months, this is clearly good news for stocks exposed to China expansion hence the leg up by Fortescue (FMG) to fresh 2-months highs, our current $20-21 target area is approaching fast.

US equities finally closed down just over 1% overnight with losses fairly evenly spread yet the SPI futures are calling the ASX slightly higher this morning continuing the outperformance from yesterday.

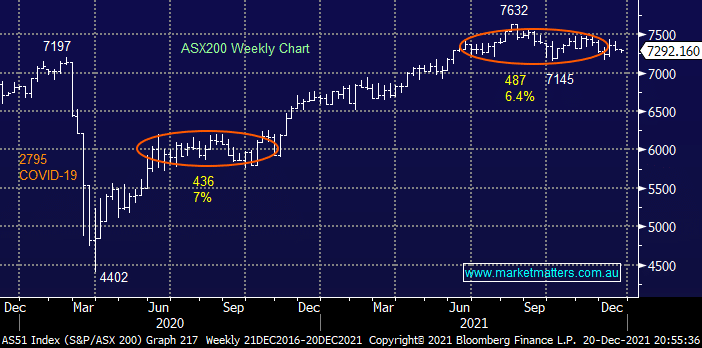

MM remains mildly bullish the ASX targeting fresh highs into 2022

Add To Hit List