Thursday saw much of the ASX200 embrace the overnight statement from the Fed but when CSL Ltd (CSL), the markets 3rd largest stock, plunges over 8% its always going to be a tough day at the office for the Australian market. However we still expected a little more from the local bourse but as MM touched on yesterday when investors are asked to stump up for $6.3bn in just 24-hours some inevitable selling will roll through other pockets of the market – yesterday it clearly wasn’t limited to healthcare names. The market would have managed a positive close if it hadn’t been for CSL and interestingly most other stocks in the sector closed up, it felt to us that any stocks that investors had been considering jettisoning from their portfolios into 2022 got the flick early!

The rotational nature of the last 12-months is continuing in earnest as Christmas approaches with bond yields acting as the conductor:

- When US bond yields stabilise or drift lower the “Big Tech” names that have dominated equities over recent years shine i.e. the FANGS & NASDAQ remain very “twitchy” to any news around inflation and yields.

- Less than 5% of the ASX200 is tech focused and most of these local names haven’t kept pace with the likes of Apple Inc (AAPL US) and Microsoft (MSFT US) hence the ASX’s underperformance compared to the US through 2021.

MM believes bond yields have peaked for a while which should be good news for tech stocks but as we saw overnight when the Bank of England (BOE) surprised the market with a rate hike big US tech got walloped even though US yields failed to react. MM feels the ASX will need other sectors to join the “Bull Party” if its going to follow the US to fresh highs with the Resources Sector our pick to take the baton. We’re still giving the uptrend the benefit of the doubt but I’m not sure we can cope with many more headwinds such as that delivered by CSL this week.

Also we feel that Omicron hasn’t finished with stocks, yesterday I enjoyed a Christmas Lunch with our website developers at Manly Wharf in Sydney, it definitely wasn’t as busy as I would have expected perhaps the soaring case numbers both here and overseas are making people more cautious i.e. record numbers in NSW and the UK in the last 24-hours are forcing us to follow politicians advice and learn to live with the virus but I cant see any exciting value in the sectors such as travel and tourism until this latest wave of uncertainty clears.

US equities experienced another mixed night with the NASDAQ weighing on other indices and general sentiment yet European stocks rallied strongly even after the UK hiked rates, it feels like investors are looking for an excuse to take profits from the high flying tech stocks. Locally the SPI is pointing to a firm opening courtesy of the resources names after commodities rallied strongly overnight i.e. copper +2.9%, crude oil +2.2% and gold +1.9%.

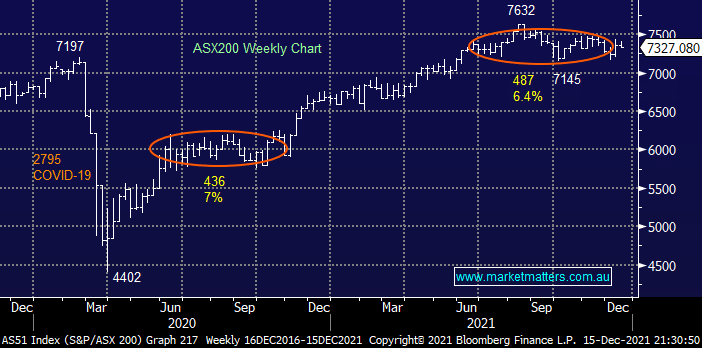

MM remains bullish the ASX targeting fresh highs into 2022

Add To Hit List