The ASX200 was clobbered 0.7% yesterday as it was unable to withstand the “Fed Jitters” – nobody’s questioning whether interest rates are headed higher both in Australia and the US but markets have become fixated with the potential speed of such hikes which will challenge many high valuation stocks and sectors. Hence it was no surprise that the IT Sector was worst on ground yesterday falling 2.6% in a session when only the Utilities stocks managed to advance. The logic is simple to comprehend although it’s not always a perfect science.

- When interest rates / bond yields increase they become a more viable option for investors – I hear almost weekly retail clients considering stocks because term deposits are paying less than 0.5% i.e. they’re delivering a negative return after inflation.

- Within the stock market itself interest rate sensitive names are likely to struggle the most, many pundits simply say the high value growth names will be rerated as bond yields increase – it certainly felt like that yesterday!

- However its good old fashioned earnings that determine a stocks performance in the long run but sentiment can clearly play an integral role month to month as we saw with tech names on Wednesday.

- Hence the “easy money” in tech may be behind us but it’s still the future hence MM believes it remains where some of the markets best successes will unfold – but there might just be more chaff than over the last decade.

US equities drifted lower into this mornings Fed decision with the tech space again on the receiving end of the most noticeable selling, the next few days appears likely to be all about the Fed and the markets interpretation of its statement as rising Omicron cases increasingly get shrugged off as old news e.g. the UK witnessed more than 78,000 cases on Wednesday, over 10,000 more than the previous highest total back in January. Stocks were already bracing for the Fed to get busy with rate hikes:

- Expectations were for policy makers to flag 2 rises next year, 3 in 2023 and 2 in 2024 taking rates up to 1.9% in 3-years’ time.

- This would have been an accelerated path than was previously outlined in September plus stimulus was also expected to be removed.

However, this morning the Fed actually were even more aggressive (hawkish) in the nearer term indicating 3 hikes in 2022 but more dovish in the outer years, i.e. the concept of more hikes now will mean that rates are lower overall into the future. Interestingly, data overnight showed that retail sales had slipped as potentially inflation is supressing spending. Stocks rallied strongly on the news as yet again we saw shorts get hammered, the concept of lower longer dated rates ever if we put up with higher rates in the short term sent the NASDAQ up 2.35%, clearly some people were very concerned around what the Fed might deliver right across the curve. The SPI futures are calling the ASX200 to recover the majority of yesterdays losses with tech likely to lead.

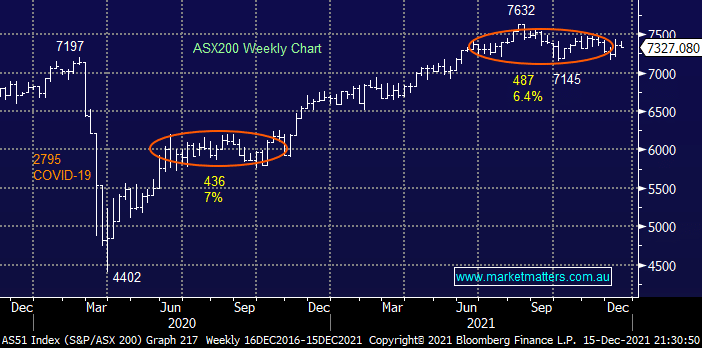

MM remains bullish the ASX targeting fresh highs into 2022

Add To Hit List