The ASX200 continues to find buying support into decent dips but it’s not yet got the stamina / belief to make any headway on the upside, yesterday saw the local market bounce over 50-points from a weak open, following an aggressive late downturn by US markets, but once it returned to unchanged the buying almost instantly became far more passive. Currently markets are transfixed on any fresh news around the Omicron variant and until we see the market hold firm on bad news the likelihood is we haven’t yet seen the end to the current nervousness, having said that we still think inflation will be back in the front of investors’ minds before we enter 2022.

There definitely appeared to be some “bargain hunting” in certain stocks & sectors on Thursday with the reopening play bouncing strongly from early losses e.g. Crown Resorts (CWN), Corportae Travel (CTD), Transurban Group (TCL) and Sydney Airports (SYD) all reversed early losses to close in positive territory even as the ASX slipped 0.15% – as we discussed in yesterday’s report MM believes accumulation of these names into current weakness will pay dividends in the weeks / months ahead.

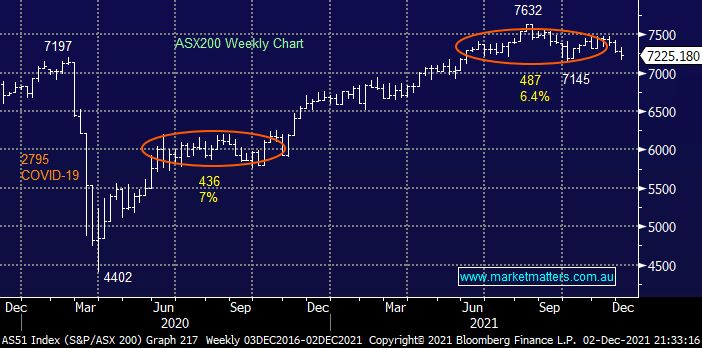

The ASX200 is actually unchanged over the last 6-months which MM feels is a touch disappointing when we weigh up the 3 major pieces of macro news over this period:

- Most of the developed world has moved on from the Delta Strain aided by surging vaccination rates i.e. over 87% of Australians and 69% of Brits have now been fully vaccinated.

- Inflation and bond yields have rallied faster than was largely forecast but not higher than most of us expected, central banks are now walking a tightrope of lifting rates while not stifling the economic recovery – rates were always going up post COVID, the only questions were when & how fast.

- Omicron has now arrived on the scene, we know its highly contagious but symptoms appear milder with the main question being how effective will current vaccines prove, and if poorly how long to develop new ones – new strains were always going to appear.

US equities rallied strongly overnight as funds migrated to the growth stocks with standout performances in the small cap and travel names, tech was the noticeable laggard after Apple (AAPL US) told its suppliers that demand for the iPhone 13 had weakened but the stock still only dipped 1% in a clear “risk on” session. The SPI futures are pointing to a strong opening this morning, up around 0.7% which will actually have the ASX trading well up for the week, it certainly doesn’t feel like it!

MM remains cautiously bullish the ASX

Add To Hit List