The ASX200 tumbled 0.6% yesterday as the banks led the broad market lower, there were a few bright pockets amongst the 30% of stocks which managed to close higher with the lithium and nickel names the standouts for me. Iron ore names are slowly getting up from the canvas on news of China easing but the tourism stocks came under distinct pressure as a number of European countries languish under an ever worsening COVID 4th wave plus yesterday evening saw Air New Zealand being been forced to cancel 1000 trans-Tasman flights due to border restrictions undoubtedly changing the plans for thousands of families for Christmas in the process.

- Germany, the Netherlands and Austria are facing harsh lockdown restrictions as the countries endure an accelerating number of COVID cases across these countries who’ve only achieved average vaccination rates – the onset of winters not helping matters.

The cyclical nature of markets never ceases to amaze me, its was only a few weeks ago that bond yields surged as higher than expected inflation data surprised analysts in many regions. The message from financial markets and the RBA was very different:

- Money markets have been targeting 3-4 rate hikes in 2022 while the RBA said they don’t anticipate raising rates until 2023 at the earliest.

- Interestingly I noticed yesterday afternoon that St George Bank had subtly dropped their fixed 3-year mortgage rate on Monday –the inflation panic may have been a touch too premature.

- Remember we’ve mentioned a few times over the last fortnight that US growth stocks had impressively ignored bond yields, perhaps they were just smarter!

Jerome Powell got the nod from Joe Biden overnight to head the Fed for another term which sent stocks and short-term bond yields higher, markets are now looking to June for the start of rate hikes but equities initially appeared relieved by the lack of surprises / unknown. Obviously this timetable could again be delayed if COVID continues to disrupt the economic expansion across the northern hemisphere.

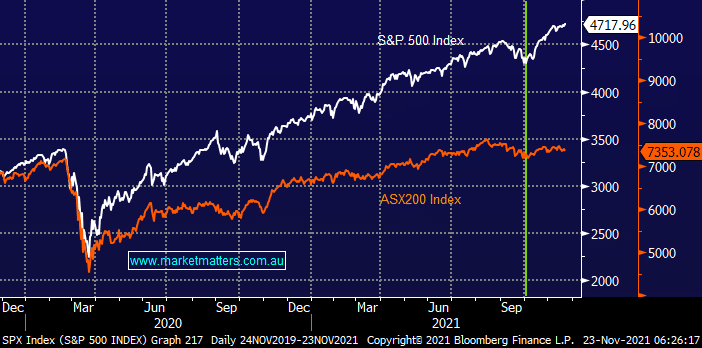

The underperformance by Australian stocks has been apparent since the COVID recovery commenced back in March 2020, primarily due to our lack of “Big Tech” however it’s become more pronounced over the last 6-weeks and although its easy to explain the whys and wherefores due to the banks and iron ore names, history tells us that when elastic bands stretch too far they have a habit of snapping back fast & hard, lets hope the time is nigh.

US stocks were mixed overnight after an aggressive late sell-off, earlier in the session all major indices registered fresh all-time highs following President Bidens decision not to rock the boat and stick with Jerome Powell as Fed Chair. However, the anticipated rate hikes from mid-2022 saw profit taking hit the tech based NASDAQ, news that the Woodside-BHP $41bn merger was set to proceed looks to have been the catalyst to send BHP Group (BHP) up strongly overseas which should help the local index only open a touch softer this morning.

MM remains bullish the ASX targeting fresh highs into Christmas

Add To Hit List