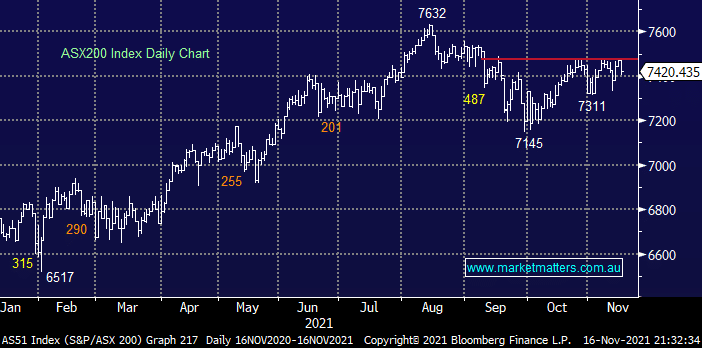

The ASX200 succumbed to broad based selling on Tuesday, only the IT Sector managed to close in positive territory while the resources led the declines – the stock and sector rotation continues almost day to day, anybody attempting to identify a clear trend looks destined for disappointment. As we often say the market will be there tomorrow and it usually tells us where it wants to go hence be patient and don’t force an opinion too firmly on this market while its treading water i.e. MM is still bullish while being conscious that the post COVID advance is maturing.

Philip Lowe & most at the RBA continue to believe that credit markets have got ahead of themselves with regard to inflation fears and rate hikes although he did sneak a standout scenario that would switch their stance – but in essence the story remains the same:

- The RBA believes there will be no rate hike (s) in 2022 while one in 2023 is a possibility, a very different picture to that currently being painted by credit markets.

- For the mortgage holders he stated that the RBA won’t be hiking rates to slow down housing prices i.e. it’s not their mandate. However the rally by 3-year bond yields has already seen fixed rates move noticeably higher.

- Wages growth appears to be the potential catalyst which “may” move the RBA to a more hawkish stance, personally I keep reading about a skills shortages in Australia driving up pay, perhaps they read different press?

At the end of yesterdays session the muted reaction by Australian bond yields and the $A to the RBA minutes from its November meeting illustrates that markets have no confidence in our central banks interpretation of the inflation story moving forward – we’re inclined to side with the bond market but an open-mind remains key as we’ve seen on a number of occasions over recent years but we believe the huge financial stimulus that’s been injected into the economic system since COVID will ultimately flow through to a meaningful increase of interest rates.

Overnight US stocks rallied strongly across the board following the largest increase in retail sales in over 6-months showing robust demand even as inflation reduced the “free cash” in people’s pockets. The fresh assault on new highs by the US S&P500 looks set to help the ASX200 recover most of yesterdays losses with the SPI calling an open up around 0.25%.

MM remains bullish the ASX targeting fresh highs in the weeks / months ahead

Add To Hit List