The ASX200 faded away yesterday following a common path over recent weeks, every time the ASX200 knocks on the 7475 door it gets sold off, no longer surprising or new – at yesterdays close the local index had only bounced 4% from its October low compared to the US S&P500’s impressive 10% rally to fresh highs. The US feels like it’s now due a rest posing the question can we buck any weakness after ignoring the strength, it does happen sometimes. The problem was 2-fold yesterday:

- The broad based market faltered with less than 40% of stocks advancing although it was more of a drift than aggressive sell-off with no sectors really catching the eye.

- The influential Banking Sector struggled after National Australia Bank (NAB) reported a mixed result, we should remember the “Big 4” have already performed a lot of heavy lifting in 2021.

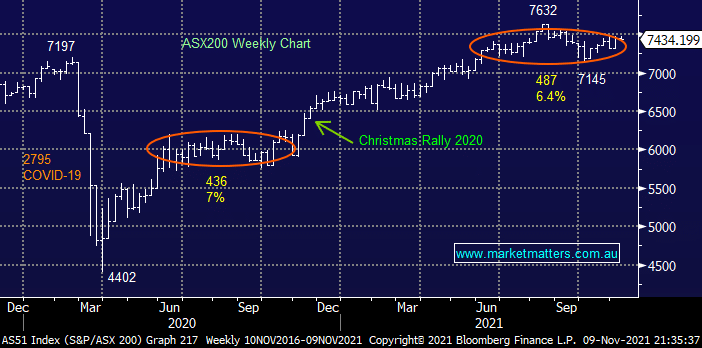

Elsewhere we simply saw ongoing sector rotation as the market hunts for direction, this time we saw strength in gold, nickel, lithium and iron ore while banks, casinos, insurance and energy names struggled. As we move towards mid-November MM feel bond yields / interest rates have largely done their dash for 2021 and the next major move on both the index level and under the hood will be a Christmas Rally as the sellers take an early holiday – my many years of experience in the market have taught me that seasonal rallies virtually always unfold but they can commence when least expected.

Overnight US stocks ended the best winning streak in 4-years as the financials fell following US 10-year bond yields to their lowest level in 7-weeks, just after local fixed home loans have been hiked. Global equities have soared on strong earnings, a post COVID reopening environment and US infrastructure spending but a 9th positive session was one step too far – they need a rest! Interestingly the SPI futures are pointing to a positive open, up around 0.2%.

MM remains bullish the ASX targeting fresh highs in the weeks / months ahead

Add To Hit List